The Great European TMS Consolidation: How 2025's Vendor Landscape Shake-Up Is Forcing Shippers to Rethink Their Procurement Strategy Before It's Too Late

The most significant TMS vendor consolidation wave in over a decade is reshaping European procurement decisions right now. WiseTech's acquisition of E2open in 2025, Descartes' purchase of 3GTMS for $115 million in March 2025, and Körber's transformation of MercuryGate into Infios following their 2024 acquisition represent just the beginning of a fundamental market restructuring that's forcing European shippers to reconsider their entire TMS procurement strategy.

The European TMS market, valued at €1.4 billion in 2024 and growing at a compound annual growth rate of 12.2 percent, is forecasted to reach €2.5 billion by 2029. This growth is happening alongside unprecedented consolidation that's eliminating choice and creating new risks for procurement teams who thought they had plenty of time to evaluate options.

The 2025 TMS Vendor Consolidation Wave That's Reshaping European Markets

The scale of recent acquisitions is staggering. Körber Supply Chain Software acquired MercuryGate International Inc., a Transportation Management System provider, to expand its supply chain execution portfolio, creating what is now known as Infios. This wasn't just a typical software acquisition; it represented a strategic move to integrate OMS, WMS, and TMS functionalities into a comprehensive supply chain platform.

Descartes Systems Group bought 3GTMS for USD 115 million in March 2025 and Sellercloud in October 2024, adding domestic planning and omnichannel order-management modules that round out end-to-end visibility. Meanwhile, WiseTech's strategic acquisition of E2open combines two of the most acquisitive players in this space, underscoring WiseTech's vision to be the operating system for global trade and logistics.

But here's what most procurement teams miss: these aren't just financial transactions. They're fundamentally altering the competitive landscape that European shippers rely on for carrier connectivity, pricing leverage, and implementation flexibility.

What These Mergers Actually Mean for Your Transport Operations

Product roadmap uncertainties are already surfacing. When two TMS platforms merge, customers inevitably face decisions about which system to standardize on, what features will be deprecated, and how long dual support will continue. E2open's recent integration into the WiseTech Global ecosystem alongside Bloom Global raises questions about its long-term neutrality. For enterprises, this acquisition may prove synergistic, but others might view it as a potential limitation.

Support structure changes follow quickly. The European mid-market manufacturers who relied on direct access to MercuryGate's development team now navigate Körber's broader supply chain portfolio, which has the potential to evolve into a more comprehensive solution but currently stands with limited international reach and basic reporting tools that could hinder adoption by larger or more global operations.

Integration timelines are extending as merged vendors focus on internal platform consolidation rather than customer-specific connectivity projects. This directly impacts European shippers whose carrier networks span multiple countries with varying technological capabilities.

The Hidden Procurement Traps European Shippers Are Walking Into

A German automotive parts manufacturer just learned what a €800,000 TMS implementation mistake looks like. They chose a North American-focused platform six months before discovering their primary carriers couldn't integrate without costly custom development. Now they're facing a complete re-implementation.

This isn't an isolated incident. According to the Standish Group's Annual CHAOS 2020 report, 66% of technology projects end in partial or total failure. Transportation management systems aren't immune to this trend. In fact, European shippers face even steeper odds due to cross-border complexities that don't exist in single-market implementations.

Research from McKinsey in 2020 found that 17% of large IT projects go so badly, they threaten the very existence of the company. The stakes are particularly high for European transport operations managing multiple regulatory frameworks, currencies, and carrier relationships across EU member states.

The most common procurement trap? Assuming that bigger means better stability. In reality, mega-vendors often prioritize their largest global accounts over European mid-market customers, leading to delayed implementations, reduced customization options, and higher total cost of ownership than initially projected.

The False Economy of 'Proven' Mega-Vendors

Feature bloat is becoming a significant issue. Blue Yonder may not be the right fit for every business. SMBs or companies simply looking for a standalone TMS might find its suite excessive both in cost and scope. Is your business prepared for a highly integrated system that covers both planning and execution?

Implementation complexity scales exponentially with platform size. Cloud TMS implementations often conclude within eight weeks, compared to 6-18 months for traditional systems. This speed difference matters when European transport regulations change frequently or when expanding into new markets. Consolidated mega-vendors typically fall into the longer implementation category due to their platform complexity and resource allocation priorities.

Cost structures favor enterprise accounts at the expense of mid-market customers. Licensed TMS software runs $50,000-$400,000+ with annual maintenance charges ranging from 15-20% of license costs. For a 100-truck operation, that initial $100,000 investment becomes $200,000+ in the first year when you factor in implementation, training, and infrastructure requirements.

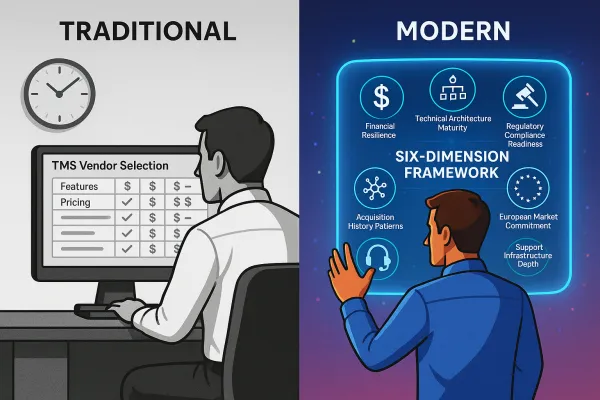

Your Strategic Framework for TMS Procurement in a Consolidating Market

European TMS procurement requires a fundamentally different approach in 2025. The traditional RFP process that worked when the market had dozens of independent vendors no longer adequately addresses consolidation risks, vendor viability concerns, or European-specific regulatory requirements.

Start with financial stability assessment. Look beyond current revenue figures to understand how recent acquisitions impact the vendor's cash flow, development priorities, and customer service capacity. Companies undergoing integration often experience 12-18 months of reduced innovation while they harmonize platforms and teams.

Evaluate European market commitment specifically. Geopolitical changes (Brexit), the scarcity of drivers and the need to retain logistics talent are some of the challenges faced by supply chain leaders in the European region. The European market typically has differentiated itself as a challenging region due to the existing fragmentation of its carrier networks, the complexity of the tariff system used by some carriers based on multiple factors and the strong localization of systems.

Demand concrete integration roadmaps. Don't accept vague promises about "best-of-breed" platform integration. Require detailed timelines for feature consolidation, data migration paths, and support structure changes. Ask specifically about their European development resources and decision-making autonomy.

The European-Specific Evaluation Criteria Most Procurement Teams Miss

Cross-border carrier connectivity isn't just about having API connections. European transport operations require deep integration with local carriers in each market, support for country-specific documentation requirements, and real-time customs and border processing capabilities.

Regulatory compliance readiness extends beyond basic eFTI support. CBAM will apply in its definitive regime from 2026, with a transitional phase of 2023 to 2025. Yet most European manufacturers are treating this like another compliance checkbox instead of the strategic opportunity it represents. If your business imports more than €150 worth of these products, you will be in scope of CBAM. Your TMS needs to handle carbon tracking, emissions reporting, and sustainability optimization as core functionality, not add-on modules.

Multi-language and multi-currency support goes deeper than interface translation. European operations require localized business logic for tax calculations, invoicing formats, and regulatory document generation that varies by country and sometimes by region within countries.

Market-by-Market Vendor Landscape Analysis: Who's Left Standing

The European TMS market is served by players such as Transporeon (now owned by Trimble), Infios (formerly Körber Supply Chain Software, including US-based MercuryGate acquired in 2024), 4flow, proLogistik, AEB, ecovium, Solvares, Soloplan and LIS based in Germany; the French groups Generix (including DDS), SINARI and AKANEA; Microlise, Aptean 3T, Mandata and HaulTech in the UK; Alpega headquartered in Austria; BlueRock TMS, Navitrans and Boltrics based in Benelux; nShift, Pagero, AddSecure and Opter in the Nordics; Inelo headquartered in Poland; the Italian companies TESISQUARE and SIMA; Alerce based in Spain; as well as AndSoft in Andorra.

The post-consolidation landscape reveals three distinct categories: global mega-vendors (Infios/MercuryGate, Descartes, SAP TM, Oracle TM, E2open/WiseTech), European specialists (Alpega, nShift, Transporeon/Trimble), and emerging European-native solutions (including Cargoson) that focus specifically on cross-border European operations.

Each category presents different risk-reward profiles. Mega-vendors offer comprehensive functionality but come with integration complexity and potential feature deprecation risks. European specialists provide market-specific knowledge but may lack global scaling capabilities. European-native solutions offer rapid deployment and local expertise but may have limited feature depth compared to enterprise platforms.

The Rise of European-Native Alternatives

European-built solutions are gaining market share precisely because they understand the unique challenges of cross-border European operations. Solutions like Cargoson focus exclusively on shippers rather than carriers or 3PLs, addressing specific challenges of manufacturing, wholesale, and retail companies. This focused approach allows for faster implementation, better carrier integration, and more responsive customer support than mega-vendors can typically provide.

Local development teams mean faster response to European regulatory changes. When eFTI requirements or carbon reporting standards change, European-native vendors can typically deploy updates within weeks rather than the months or quarters required by global platforms that must prioritize changes across multiple regions.

Pricing models also tend to favor European mid-market customers. Cloud TMS pricing ranges from $1.00 to $4.00 per freight load booked in the system. For many European shippers, this translates to predictable monthly costs that scale with business growth rather than fixed infrastructure investments.

Implementation Strategy for a Post-Consolidation World

Successful TMS implementations in the current market require different strategies than they did even two years ago. Companies succeed because they treat the project as business transformation, not software implementation. They allocate budget for extensive change management, hire European transportation consultants who understand both the software and local market requirements, and give their implementation team authority to make decisions across subsidiaries.

Contract negotiations must address consolidation risks explicitly. Include clauses that protect against feature deprecation, require advance notice of platform changes, and guarantee data portability in standard formats. Specify European support requirements and local language capabilities that cannot be reduced without customer consent.

Phased deployment approaches reduce vendor lock-in risks while allowing you to evaluate platform performance before full commitment. The most successful migrations follow a phased approach: pilot with one major lane, measure results carefully, then expand systematically. Current favorable European transport market conditions make this an optimal time to negotiate better platform terms and carrier partnerships.

Data ownership and integration standards deserve particular attention. Ensure your contract specifies complete data ownership, requires API access for all functionality, and mandates export capabilities in industry-standard formats. This protects against future vendor changes while enabling integration with complementary systems.

Future-Proofing Your TMS Investment Against Further Consolidation

The consolidation wave isn't over. Additional acquisitions are likely as private equity firms and strategic acquirers seek to capture market share in the growing European TMS market. Your procurement strategy must account for ongoing vendor landscape changes.

API-first architecture requirements protect against platform changes by ensuring your integrations don't depend on proprietary connections that may be deprecated during vendor consolidations. Specify open API standards and require documentation that enables third-party integration development.

Multi-vendor strategies can provide insurance against individual vendor risks, though they require more complex integration management. Consider core TMS functionality from your primary vendor with specialized modules (carbon tracking, customs management, carrier connectivity) from best-of-breed providers that integrate via APIs.

The European TMS vendor consolidation of 2025 represents both challenge and opportunity. Companies that understand the new landscape, evaluate vendors based on post-consolidation criteria, and implement with appropriate risk mitigation will emerge with competitive advantages. Those that treat vendor selection as a traditional software purchase may find themselves facing expensive re-implementations within 24 months.

Your next TMS decision may be your most important transport technology choice of the decade. Choose carefully, but don't delay. The vendor landscape will look dramatically different by 2026.