The European Shipper's TMS Vendor Consolidation Survival Guide: How to Secure Acquisition-Resistant Procurement Contracts Before 2026's Market Reshuffling Eliminates Your Best Technology Options

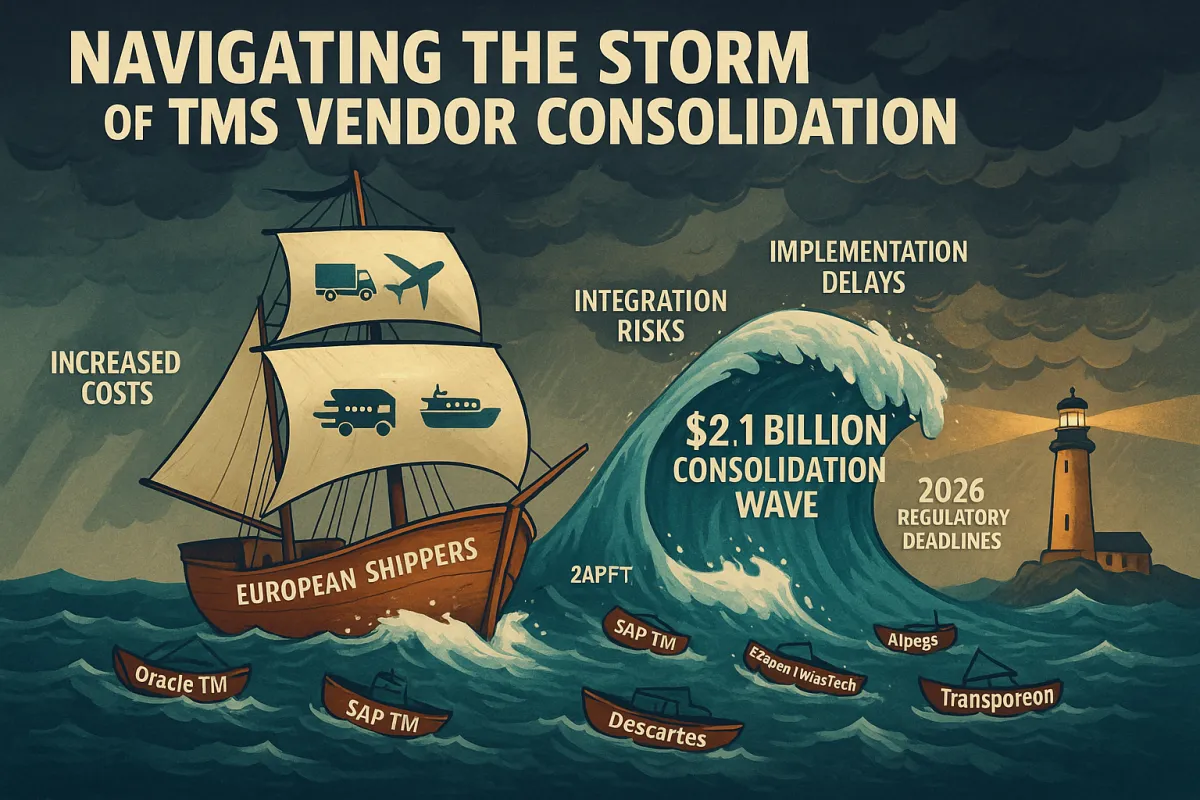

WiseTech Global's $2.1 billion acquisition of E2open signals the beginning of an unprecedented consolidation wave that European shippers can't ignore. European shippers face a sobering reality: 66% of technology projects end in partial or total failure, and now you're forced to navigate TMS vendor consolidation while meeting 2026's regulatory deadlines.

The timing creates a perfect storm. 76% of logistics transformations never meet their budget, timeline, or performance targets, yet European manufacturers face mandatory compliance requirements that leave no room for implementation delays. Your procurement decisions in the next six months will determine whether you secure a stable, regulation-ready platform or join the growing list of budget disasters plaguing reactive strategies.

The €2.1 Billion Consolidation Wave Reshaping European TMS Options

WiseTech's acquisition of E2open for $2.1 billion, Descartes' purchase of 3GTMS for $115 million, and the deal marks Descartes' 32nd acquisition since 2016 represent only the visible portion of a market restructuring that's eliminating vendor choice faster than most procurement teams realize.

The post-consolidation landscape reveals three distinct categories: global mega-vendors (Oracle TM, SAP TM, E2open/WiseTech, Descartes), European specialists (Alpega, nShift, Transporeon), and emerging European-native solutions like Cargoson that maintain development focus specifically on European regulatory requirements. Each category presents fundamentally different risk profiles for your procurement strategy.

Here's what most procurement teams miss: Companies undergoing integration often experience 12-18 months of reduced innovation while they harmonize platforms and teams. When your vendor becomes an acquisition target, you inherit integration risks and delays without managing the project directly.

Timeline pressure intensifies beyond 2026. Companies that haven't initiated TMS selection processes by mid-2026 will find significantly fewer viable options as consolidation eliminates redundant platforms and development resources get redistributed to integration priorities rather than customer-specific enhancements.

Why Standard TMS Contracts Leave European Shippers Vulnerable

Standard TMS contracts rarely address vendor acquisition scenarios, leaving you exposed to post-acquisition service degradation that can derail operations. When their vendor introduced eFTI compliance as a premium add-on module nine months later, the additional licensing costs reached €800,000 annually for one German automotive parts manufacturer who learned this lesson the expensive way.

Traditional procurement frameworks evaluate vendors based on current functionality and pricing, but standard vendor scoring frameworks built around feature checklists, pricing comparisons, and current functionality miss the consolidation risks that now define procurement success.

Real costs of vendor transitions multiply when platforms merge. Implementation delays stretch to 12-18 months while acquired companies restructure support teams, and pricing often increases during "harmonization" periods when vendors eliminate competitive pressure between their newly combined platforms.

The 76% Implementation Crisis Amplified by Market Consolidation

76% of logistics transformations never meet their budget, timeline, or performance targets, but consolidation amplifies these risks through implementation complexity that traditional methodologies can't handle. A German automotive parts manufacturer discovered their €800,000 TMS implementation mistake the hard way when they realized six months into deployment that their chosen platform couldn't handle cross-border European operations.

The math is stark: 73% of discrete manufacturing ERP projects fail to meet their objectives, with average cost overruns reaching 215%. While these numbers reflect ERP implementations, TMS projects in manufacturing environments face similar complexity multipliers.

Vendor consolidation increases implementation risks through resource allocation changes. When two companies merge, customer-facing teams get reassigned to integration projects, leaving existing customers with reduced support during their own implementations. This creates cascading delays that most project timelines don't anticipate.

The Hidden Costs Multiplying During Market Transitions

Base licensing typically represents 20-30% of total costs, implementation expenses 25-40%, carrier integration fees 15-25%, ongoing support and maintenance 10-15%, and capacity shortage contingencies 5-10% additional buffer. These numbers reflect current market conditions before consolidation pressures increase pricing power.

Implementation complexity scales exponentially with European operations. A basic domestic shipper needs 10-15 integrations minimum, totaling 1,000-1,500 hours of labor, while most shippers today require an average of 40 integrations. Cross-border operations multiply this complexity through varying carrier protocols and regulatory requirements by country.

Plan for 15-20% budget increases in 2026-2027 if reactive, or 8-12% if proactive with proper contract protection. The difference reflects procurement leverage available before consolidation eliminates competitive pressure between formerly independent vendors.

Building Acquisition-Resistant Procurement Frameworks

Acquisition-resistant contracts require specific protections that standard TMS agreements ignore. Acquisition-resistant contracts require specific protections including 12-18 months advance notice for ownership changes, guaranteed functionality preservation for minimum periods, and migration assistance rights. Include specific clauses requiring 12-18 months advance notice of ownership changes, with automatic contract review rights triggered by acquisition announcements.

Price protection clauses should lock pricing for 24 months following ownership changes, preventing immediate cost increases during integration periods when you have limited negotiation leverage.

Due diligence criteria must evaluate vendor financial stability and acquisition risk beyond traditional technology assessments. Review ownership structures, debt levels, and market positioning to identify potential acquisition targets. Vendors with private equity ownership or declining market share face higher acquisition probability than established market leaders.

Multi-vendor strategies provide protection through reduced dependency risk, but implementation complexity increases significantly. Consider hybrid approaches where core functionality relies on stable platforms while specialized European compliance features utilize regional vendors with stronger regulatory focus.

European Regulatory Compliance as Procurement Leverage

eFTI compliance creates procurement leverage that won't repeat once vendors establish their approaches. As of January 2026, eFTI platforms and service providers can start preparing for operations while Member States authorities may start accepting data stored on certified eFTI platforms for inspection. From 9 July 2027, all national authorities will be obliged to accept freight documentation in electronic form via certified eFTI platforms.

From July 1, 2026, vans weighing 2.5-3.5 tons performing international transport of goods will be subject to the obligation to use second-generation smart tachographs (G2V2). Use this deadline as a contract delivery milestone with penalty clauses for non-compliance.

The regulatory convergence creates natural negotiation points. Vendors claiming regulatory readiness should demonstrate functional integration by January 2026, not just promise compliance by the July 2027 mandate. This timeline separation allows you to evaluate actual capabilities rather than marketing promises.

Strategic Vendor Evaluation in a Consolidated Market

The post-consolidation landscape reveals three distinct categories: global mega-vendors (Oracle TM, SAP TM, E2open/WiseTech, Descartes), European specialists (Alpega, nShift, Transporeon), and emerging European-native solutions like Cargoson that maintain development focus specifically on European regulatory requirements. Each category offers different risk-reward profiles for long-term strategy planning.

Global mega-vendors provide comprehensive functionality and financial stability, but traditional providers like SAP TM and Oracle often struggle with localized European requirements. Their conversational AI modules are built for global markets, which means they lack the nuanced understanding of European transport corridors, seasonal capacity variations, and regulatory differences between EU member states.

Technical capability assessment during consolidation uncertainty requires evaluating actual integration timelines rather than theoretical capabilities. Integration timelines are extending as merged vendors focus on internal platform consolidation rather than customer-specific connectivity projects.

Reference customer validation becomes critical when evaluating post-acquisition track records. Contact customers who experienced vendor transitions to understand actual service level impacts during integration periods, not just marketing case studies highlighting successful outcomes.

The European-Native Advantage During Market Disruption

European-native TMS vendors provide inherent protection against consolidation disruption through focused market positioning and regulatory alignment. SAP TM dominates German operations, MercuryGate focuses heavily on North American markets, while Alpega and Cargoson compete more directly for cross-border European business. Regional vendors typically offer faster regulatory response times for European compliance requirements.

Cargoson, Alpega, and other European specialists maintain development resources focused exclusively on European market needs, while global vendors like Descartes or WiseTech spread development efforts across multiple geographic priorities. This focus translates into faster feature development for European-specific requirements and more responsive customer support during regulatory transitions.

European-native solutions like Cargoson and Alpega understand GDPR and data residency requirements inherently rather than treating them as compliance burdens. GDPR and data residency requirements favor EU private clouds over global platforms, creating natural advantages for vendors with European-focused architectures.

Implementation Timeline Strategies for 2026-2027

European regulatory timelines provide natural implementation phases: core functionality validation in Q2-Q3 2025, eFTI readiness by January 2026, G2V2 integration by July 2026. This phased approach controls risk while meeting compliance deadlines without rushing critical integrations.

TMS implementation usually takes 1-2 months for smaller shippers and 3-6 months for a larger, more complex network. Digital transformation is reshaping the business world, with a staggering 91% of businesses embarking on digital initiatives. However, successful digital transformation is challenging, as evidenced by the fact that only 16% of organizations report success in their digital transformation efforts, often hindered by poor digital adoption rates.

Plan for 8-12 months to implement properly despite vendor claims about rapid deployment timeframes. Baseline functionality in 6-8 weeks is realistic. Full value realization (integrations, training, adoption, process change) takes 4-6 months minimum.

Avoid the rush while securing favorable terms by initiating procurement processes before Q1 2026. The procurement window for securing optimal TMS platforms before vendor consolidation eliminates choices and capacity shortages worsen cost structures runs through Q1 2026. Companies that delay face reduced vendor options and increased pricing as consolidation eliminates competitive pressure.

Your procurement decisions in the next six months determine whether you navigate 2026's regulatory requirements with a stable, acquisition-resistant platform or join the statistics of failed implementations and budget overruns that plague reactive strategies. Start your vendor evaluation now while options remain available and leverage exists for favorable contract terms that protect against consolidation risks.