The European Mid-Market Manufacturer's TMS Implementation Crisis: How to Navigate Vendor Consolidation and Triple Regulatory Deadlines Before 2026's Perfect Storm Eliminates Your Best Options

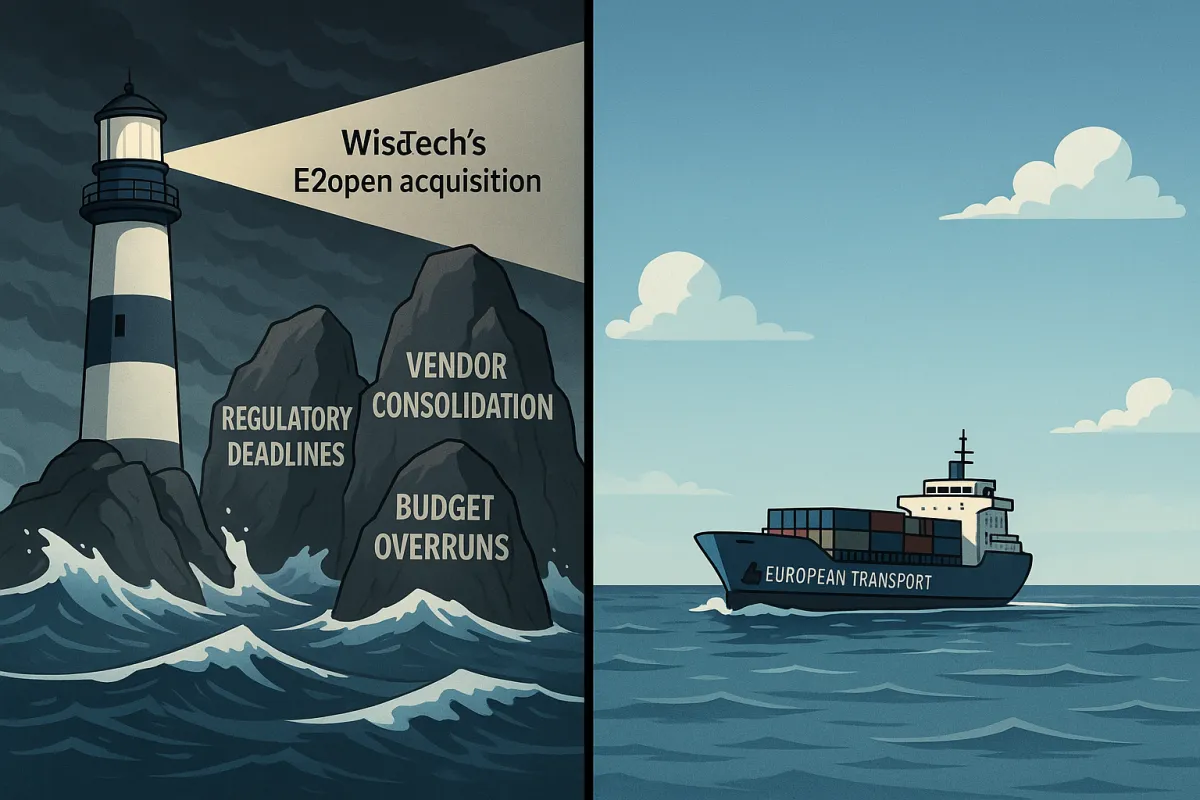

European mid-market manufacturers planning TMS implementations before the anticipated completion of WiseTech's E2open acquisition in 1H26 face a convergence of pressures that creates what industry analysts call the "perfect storm" of transport technology procurement. Budget overruns hit 75% of European TMS implementations while regulatory deadlines approach simultaneously, vendor options disappear through consolidation, and 66% of technology projects end in partial or total failure.

The timing creates unique risks for companies managing annual transport spends above €10 million. By 9 July 2027, the eFTI Regulation will apply in full, requiring Member State authorities to accept information shared electronically via certified eFTI platforms, while CBAM obligations take effect from 1 January 2026, with the first annual declaration and certificate surrender due by 30 September 2027 for all 2026 imports. These aren't optional upgrades you can postpone when budgets tighten.

The 2026 Perfect Storm: When Regulatory Pressure Meets Vendor Consolidation

The regulatory landscape creates three simultaneous compliance requirements that transform TMS from operational improvement to mandatory infrastructure. Although the definitive CBAM period commences on 1 January 2026, importers will be able to purchase certificates from February 2027 to cover CBAM goods imported in 2026, creating a retroactive financial obligation that demands accurate emissions tracking throughout the year.

As of January 2026, eFTI platforms and service providers can start preparing for operations, while by December 2026, the Commission plans to adopt the remaining eFTI implementing specifications providing detailed functional and technical requirements for IT systems and certification rules. Transport management systems claiming future compliance need to demonstrate functional integration during 2026, not merely promise readiness by the July 2027 deadline.

The G2V2 tachograph mandate adds another layer. Starting 19 August 2025, all heavy-duty vehicles registered in the EU and operating in Member States other than their Member State of registration must be fitted with G2V2 devices. This creates massive data streams requiring automated processing rather than manual analysis.

The Vendor Consolidation Reality: Why Traditional Procurement Approaches Are Failing

WiseTech's $2.1 billion acquisition of E2open represents the largest in its history, while Descartes' deal for 3GTMS marks the 32nd acquisition by the company since 2016. The scale matters because these acquisitions create integration periods where when your TMS vendor becomes an acquisition target, you inherit integration risks without managing the project, with post-acquisition integration timelines typically spanning 12-18 months while platform development stagnates.

WiseTech completed the acquisition of E2open for $3.30 per share in cash equating to an enterprise value of $2.1 billion, fully debt funded from a new syndicated debt facility. The transaction closed in August 2025, meaning integration disruption is happening right now for existing customers of both platforms.

Companies evaluating Oracle TM or SAP TM discover these global platforms often struggle with European-specific requirements compared to regional specialists. Consider Cargoson alongside consolidated platforms like Oracle TM or Blue Yonder - European-native vendors often provide better insulation against global consolidation dynamics while maintaining specialized corridor expertise.

This procurement window runs through Q1 2026, after which your leverage disappears as regulatory pressure forces decisions. Vendors shift resources toward supporting existing customers through compliance requirements rather than competing for new implementations.

The Mid-Market Integration Trap: Why 75% of Projects Exceed Budget

Legacy ERP integration challenges hit mid-market companies disproportionately hard because they lack internal expertise to manage complex system integrations, while basic API integrations cost €5,000-€15,000 and complex ERP connections exceed €50,000. But the real shock comes when you discover the full scope.

Enterprises running SAP ECC or Oracle E-Business Suite incur integration bills of USD 500,000 to USD 3 million when layering a cloud TMS, as legacy systems lack modern APIs. Mid-market manufacturers typically operate multiple legacy systems requiring custom integration work that vendors exclude from initial quotes.

European manufacturers discover that a basic domestic shipper requires 10-15 integrations minimum, potentially totaling 1,000-1,500 hours of labor, while for shippers with freight spend exceeding $250M annually, implementation can cost 2-3 times the subscription fee.

API-first platforms like Cargoson reduce integration complexity through pre-built connections, while legacy EDI approaches require custom development for each carrier relationship. The architectural choice you make determines whether integration costs remain predictable or spiral beyond budget projections.

Most shippers today require an average of 40 integrations, spanning carrier connections, customs systems, telematics platforms, and internal ERP systems. Each connection requires testing, documentation, and ongoing maintenance that compound implementation costs.

The Acquisition-Resistant Procurement Framework: 5 Critical Protection Strategies

Standard TMS contracts fail during vendor acquisitions because they don't address ownership changes or platform integration risks. European buyers need specific protections that traditional procurement frameworks miss.

1. Acquisition Notification Requirements: Include acquisition notification requirements, price protection clauses, functionality guarantees, and termination rights in contract terms negotiation focused on consolidation protection. Require 12-18 months advance notice of any ownership changes affecting your contract terms.

2. Platform Continuity Guarantees: Negotiate guaranteed functionality preservation during integration periods. When WiseTech acquired E2open, existing customers faced uncertainty about which platform features would survive the merger. Contract language should specify that core functionality remains unchanged for at least 24 months following any acquisition.

3. Price Protection During Transitions: Lock pricing for 24 months following ownership changes. Acquiring companies often rationalize pricing across acquired platforms, typically upward. Build protection against "alignment" increases that penalize loyal customers.

4. Migration Assistance Rights: Include rights to vendor-supported migration if platform consolidation creates unacceptable service disruption. This provides exit options when integration creates operational problems you can't control.

5. European Regulatory Compliance Continuity: Specify that regulatory compliance features cannot be deprecated during platform integration. eFTI and CBAM compliance requirements are non-negotiable for European operations, regardless of global platform priorities.

European specialists maintain development resources focused exclusively on European market needs, while global vendors spread development efforts across multiple geographic priorities, translating into faster feature development for European-specific requirements and more responsive customer support during regulatory transitions.

The European-Specific Compliance Advantage: Regulatory Requirements as Vendor Selection Criteria

Vendors claiming eFTI readiness should demonstrate functional integration by January 2026, not just promise compliance by July 2027. As of January 2026, eFTI platforms and service providers can start preparing for operations, while Member States authorities may start accepting data stored on certified eFTI platforms for inspection.

European TMS vendors like Alpega and Cargoson typically offer advantages through dedicated European development teams focused on regional compliance requirements. Consider Cargoson alongside consolidated platforms - European-native vendors often provide better insulation against global consolidation dynamics while maintaining specialized corridor expertise.

Platforms like Cargoson, Manhattan Active, MercuryGate, and Descartes each bring different approaches to ICS2 compliance, but European-native solutions often provide better understanding of cross-border complexity and multi-country regulatory variations. This regional expertise becomes critical when managing transport operations across multiple EU jurisdictions with varying implementation approaches.

Global platforms like Oracle TM and SAP TM often treat European compliance as an add-on module rather than core functionality. The development priority gap becomes apparent when urgent regulatory updates require immediate platform modifications. European-focused vendors typically deliver compliance features months before global competitors.

Implementation Timeline Strategy: The Q1 2026 Procurement Window

This procurement window runs through Q1 2026, after which your leverage disappears as regulatory pressure forces decisions. The timing creates urgency, but rushed decisions amplify both costs and risks.

Start with core functionality in Q2-Q3 2025, activate AI features in Q4 2025, and ensure eFTI compliance by Q1 2026. This phased approach allows validation of basic functionality before adding compliance complexity.

TMS implementation usually takes 1-2 months for smaller shippers and 3-6 months for larger, more complex networks. European mid-market manufacturers typically fall between these timeframes due to cross-border complexity combined with smaller operational scale than enterprise implementations.

Contract negotiations should include specific milestones tied to regulatory deadlines. These regulatory deadlines create negotiation leverage that savvy buyers can exploit for better contract terms and protection against vendor lock-in, as your leverage is strongest when vendors need your commitment to justify their development investments.

Establish 60-day checkpoints to validate integration progress and cost tracking. Monitor carrier onboarding speed, data quality metrics, and user adoption rates to identify budget risks before they become disasters.

Future-Proofing Your Decision: Building Resilience for Post-2027 Operations

The post-2030 transport landscape rewards organizations building resilient, adaptable systems during the current infrastructure crisis. The Europe Telematics Market size is estimated at 24.49 million units in 2025, expected to reach 49.77 million units by 2030, with the number of active telematics devices reflecting not a trend but a structural shift.

Your TMS architecture must handle this data explosion through automated processing rather than manual analysis. QR code generation and machine-readable format requirements become mandatory by July 2027, requiring your TMS to generate these automatically for every shipment across all transport modes.

Vendor diversification strategies protect against future consolidation waves. The current consolidation represents the beginning, not the end, of market restructuring. This aggressive acquisition pattern indicates further consolidation ahead, not behind us.

European-native vendors provide strategic options that remain independent of global consolidation dynamics. Platforms like Cargoson, Alpega, and other regional specialists maintain European operational focus that mega-vendors often dilute post-acquisition.

Build compliance automation capabilities that adapt to regulatory changes without requiring platform migration. eFTI implementation brings estimated cost savings of up to €1 billion per year for the EU transport and logistics sector through more efficient logistical planning and improving supply chain predictability and resilience while enhancing interoperability between transport networks.

The measurement frameworks you build today determine competitive position post-2026. While competitors focus on squeezing carrier rates, forward-thinking shippers discover that TMS productivity gains deliver more competitive advantage than cost negotiations when Europe's driver shortage constraints limit traditional procurement approaches.

European shippers who act decisively within the next 90 days position themselves to navigate 2026's perfect storm successfully, while those who delay risk joining the statistics of failed implementations and budget overruns plaguing reactive procurement strategies.