The European Shipper's Multimodal TMS Resilience Strategy: How to Build Corridor-Adaptive Transport Management That Thrives Despite TEN-T Delays While Securing Vendor-Resilient Platforms Before 2026's Consolidation Window Closes

European manufacturers managing €50+ million transport operations thought they had problems when average delays of 17 years for five of the assessed projects emerged from the latest European Court of Auditors report. That was before WiseTech Global completed the acquisition of E2open for $2.1 billion and Descartes Systems Group acquired 3GTMS for $115 million, marking Descartes' 32nd acquisition since 2016. You're facing the perfect storm: infrastructure that won't work when promised, vendor consolidation eliminating your negotiation leverage, and regulatory deadlines that won't wait.

The numbers paint a stark picture. The eight megaprojects had experienced an overall real cost increase of 47% against original estimates in 2020, but today the difference is almost twice as high, at +82%. Meanwhile, Rail Baltica has seen the most dramatic cost escalation, with its budget increasing by 291% compared to its original estimate, rising from €4.6 billion to €18.2 billion. Your multimodal transport management strategy must account for infrastructure that's hemorrhaging budgets and timelines while your vendor options disappear through acquisition waves.

The €515 Billion Infrastructure Reality Check

The EU auditors have changed their assessment of the 2030 goal for the completion of the core Trans-European Transport Network (TEN-T) from "unlikely to be met" five years ago to a clear "will not be met" now. Here's what this means for your multimodal transport planning: every corridor-dependent strategy you've built assumes infrastructure connectivity that simply won't exist by 2030.

Consider the scale of these delays. The opening of the Lyon-Turin rail link is now forecast for 2033, rather than the original goal of 2015 or revised one of 2030; the Brenner Base Tunnel is now expected to open at the earliest in 2032, not in 2016 or 2028. For a German automotive manufacturer shipping through these corridors, this doesn't just mean delayed efficiency gains—it means your entire modal shift calculations are wrong.

The Community of European Railway and Infrastructure Companies (CER) said that completing the TEN-T required "massive investments" – €500 billion by 2030 and €1,500 billion by 2050. Yet procurement teams continue building TMS requirements around infrastructure completion dates that auditors now describe as fantasy. Your system architecture must accommodate persistent fragmentation, not eventual connectivity.

Smart European shippers are flipping this constraint into an advantage. While competitors wait for infrastructure completion, you can build multimodal strategies that thrive on fragmentation. Your TMS selection should prioritize systems that excel at connecting disparate networks rather than waiting for seamless corridors.

The Vendor Consolidation Crisis

Market consolidation has accelerated beyond traditional procurement planning cycles. WiseTech's most ambitious step came in 2024 with the $2.1 billion acquisition of E2open—the largest in its history, while Descartes' deal for 3GTMS is the 32nd acquisition by the Waterloo, Ontario-headquartered company since 2016, with Columbus, Ohio-based 3GTMS providing automation for planning, rating, consolidation and routing of over-the-road shipments.

Here's the procurement reality most teams miss: when your TMS vendor becomes an acquisition target, you inherit integration risks without directly managing the project, with post-acquisition integration timelines typically spanning 12-18 months. During these periods, platform development stagnates while resources get redirected to harmonizing systems.

The timing creates additional pressure. This procurement window running through Q1 2026—after which your leverage disappears as regulatory pressure forces decisions. Companies that haven't initiated TMS selection processes by mid-2026 will find significantly fewer viable options as vendors focus on existing customer compliance rather than new acquisitions.

European shippers need vendor strategies that account for this consolidation reality. Consider Cargoson alongside consolidated platforms like Oracle TM, Blue Yonder, or the newly combined WiseTech/E2open entity. European-native vendors often provide better insulation against global consolidation dynamics while maintaining specialized corridor expertise.

Corridor-Specific Digital Integration

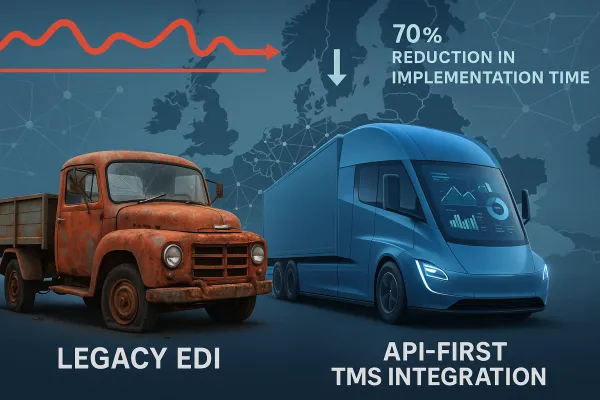

Infrastructure fragmentation demands sophisticated data harmonization across incompatible systems. You can't wait for ERTMS standardization when each national rail system operates different data protocols. Your TMS must excel at normalizing disparate information streams rather than assuming seamless connectivity.

The regulatory environment supports this approach. As of January 2026: eFTI platforms and service providers can start preparing for operations. Member States authorities may start accepting data stored on certified eFTI platforms for inspection. This creates an implementation window for building data integration capabilities before by 9 July 2027, Member States must accept electronic freight information via certified eFTI platforms.

Smart procurement teams are leveraging this timeline. Build TMS capabilities around API management and data normalization during 2025-2026, positioning your organization to benefit from eventual corridor completion while thriving during continued fragmentation. Evaluate platforms based on their ability to connect fragmented networks, not just their efficiency within integrated systems.

Compare multimodal data integration across vendors like MercuryGate (now part of Körber's Infios), Manhattan Active, and European specialists. Look for proven experience managing cross-border data complexity rather than promises of future seamless integration.

Risk Mitigation Framework

Effective multimodal resilience requires contingency-first architecture. Your TMS should automate modal shifts when infrastructure constraints emerge, manage capacity shortages across multiple networks, and integrate geopolitical risk monitoring that affects corridor availability.

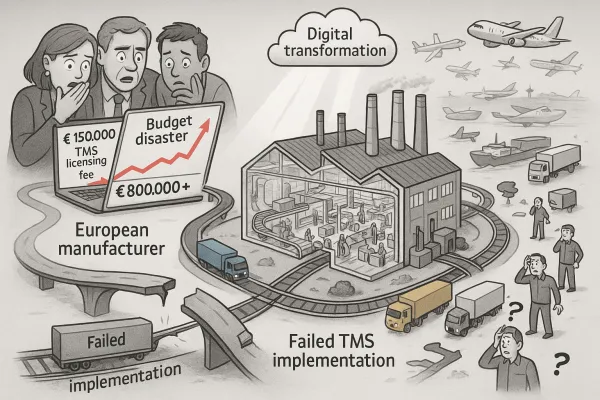

A practical example: Dutch food distributors discovered during 2024's Rhine shipping disruptions that their TMS couldn't rapidly shift volumes to rail alternatives when water levels dropped. The platforms that performed best had built-in marketplace integration and real-time alternative routing capabilities.

When evaluating vendors, test contingency scenarios during demonstrations. How quickly can the system identify and book alternative capacity when your primary corridor experiences delays? Does the platform connect to spot markets automatically, or require manual intervention?

Consider platforms that integrate transport marketplaces natively. FreightPOP, Uber Freight, and Cargoson offer built-in marketplace connectivity versus traditional enterprise solutions that require separate integration projects. This architecture provides automatic fallback capacity when primary arrangements fail.

Implementation Timeline: The 90-Day Window

Market dynamics create a narrow procurement window. Those who delay face increasingly limited options as regulatory deadlines approach and vendor acquisition activity accelerates. Your 90-day implementation framework should address corridor assessment, vendor evaluation, and contract protection before options narrow further.

Phase 1: Corridor Assessment (Days 1-30)

Document your critical transport corridors and their TEN-T dependencies. Map which routes rely on delayed infrastructure projects and identify alternative modal combinations. Quantify the cost impact of continued fragmentation versus eventual completion.

Phase 2: Vendor Evaluation (Days 31-60)

Evaluate platforms based on multimodal resilience capabilities. Compare Oracle TM, SAP TM, and the WiseTech/E2open combination against European specialists like Alpega, Transporeon, and Cargoson. Focus on proven fragmentation management rather than corridor optimization features.

Phase 3: Contract Protection (Days 61-90)

Structure agreements with acquisition-resistant terms. Include specific language requiring 12-18 months advance notice of any acquisition discussions, price protection during ownership transitions, and functionality guarantees that prevent feature deprecation without equivalent replacement.

Regulatory Leverage: Using 2026 Compliance Deadlines

European regulatory timelines create natural negotiation leverage points that smart procurement teams are exploiting. From 1 July 2026, international freight transport performed by vans up to 3.5 tonnes enters the tachograph regime: second-generation smart tachographs (G2V2) become mandatory, affecting thousands of light commercial vehicles across Europe, while the deadlines include ADR enforcement by June 2026, G2V2 tachographs for vans by July 2026, digital ECMT permits from January 2026, and progressive eFTI platform certification starting January 2026.

Vendors face the same compliance deadlines with greater customer exposure. Use this pressure to secure better contract terms, implementation support, and compliance guarantees. European-focused vendors like Cargoson, Alpega, and nShift often provide stronger regulatory response compared to global platforms treating European compliance as secondary requirements.

The eFTI implementation timeline offers specific negotiation windows. From January 2025: Member States can start setting up the IT infrastructure needed to handle eFTI-compliant transport information. By September 2025: the European Commission plans to finalize additional specifications. Demand functional eFTI integration during this preparation phase rather than promises for the July 2027 deadline.

Future-Proofing Strategy

Build systems that benefit from eventual infrastructure completion while surviving continued delays. Your TMS architecture should scale upward when corridors finally connect while maintaining efficiency during persistent fragmentation. This requires scalable data management, AI-ready automation frameworks, and vendor relationships that prioritize European market development.

Consider the long-term vendor viability across different categories. Consolidated mega-vendors offer comprehensive functionality but may deprioritize European-specific features. European specialists provide market focus but may lack global scaling capabilities. Evaluate the balance based on your specific corridor dependencies and growth plans.

The post-2030 transport landscape will reward organizations that built resilient, adaptable systems during the current infrastructure crisis. Your procurement decisions in 2025-2026 determine whether you're positioned to capitalize on eventual corridor completion or trapped by reactive technology choices that assume infrastructure reliability that doesn't exist.

Start your corridor-adaptive TMS evaluation now. The vendor landscape will look dramatically different by 2026, and the infrastructure problems aren't going anywhere soon. Your competitive advantage depends on building multimodal resilience that thrives on European transport reality rather than waiting for Brussels' promises to materialize.