The European Mid-Market TMS Adoption Crisis: How to Overcome the 5 Critical Barriers Preventing Implementation Success Before Vendor Consolidation and Regulatory Deadlines Eliminate Your Options

European manufacturers managing transport operations worth €10 million or more annually face an uncomfortable truth. Despite the Transportation Management System market reaching maturity in many respects, mid-sized shippers deploy cloud-based TMS solutions at only 62% penetration rates, while North America held the largest regional share in 2025 at 42.67% showing dramatic geographical disparities in adoption.

66% of technology projects end in partial or total failure, with 17% of large IT projects threatening company existence. Budget overruns hit 75% of European TMS implementations, and these statistics are worsening precisely as regulatory pressure forces mandatory digital transformation. The timing couldn't be worse. WiseTech's acquisition of e2open for $3.30 per share in cash equating to an enterprise value of $2.1 billion marks the largest TMS industry acquisition to date, while Descartes Systems Group has acquired Columbus, Ohio-based 3Gtms for $115 million USD in cash, reshaping vendor options for European buyers.

The 2026 Regulatory Pressure Multiplier

The regulatory convergence happening now amplifies every existing TMS adoption barrier. From July 1, 2026, vans weighing 2.5-3.5 tons performing international transport of goods will be subject to the obligation to use second-generation smart tachographs (G2V2). Simultaneously, as of 1 January 2026, the transitional phase of the Carbon Border Adjustment Mechanism (CBAM) has ended and the definitive phase has begun with importers now subject to full financial obligations under the scheme.

As of 9 July 2027, the eFTI Regulation will apply in full, creating a compressed implementation window that most procurement teams underestimate. By July 2027, all Member States will be required to accept electronic transport data via eFTI-certified platforms, making 2026 the critical preparation year.

For companies importing carbon-intensive goods, the cost of non-compliance is now substantial. From 1 January 2026 importers must purchase and surrender certificates based on verified annual emissions, with a €100 per excess tonne penalty for non-compliance. Compare this to TMS implementation costs, and the regulatory compliance argument becomes compelling for procurement committees still debating investment timing.

Barrier #1: The True Cost Calculation Crisis

Mid-market companies systematically underestimate TMS total cost of ownership, and the consequences are brutal. European manufacturers are discovering that a basic domestic shipper requires 10-15 integrations minimum, potentially totaling 1,000-1,500 hours of labor. For shippers with freight spend exceeding $250M annually, implementation can cost 2-3 times the subscription fee.

The hidden costs go beyond basic integration. Enterprises running SAP ECC or Oracle E-Business Suite incur integration bills of USD 500,000 to USD 3 million when layering a cloud TMS, as legacy systems lack modern APIs. Your CFO sees the subscription fees—typically €1-4 per shipment for cloud solutions—but misses the integration reality.

A German automotive manufacturer learned this lesson expensively. In early 2024, they signed a three-year TMS renewal without regulatory compliance pricing protection. When their vendor introduced eFTI compliance as a premium add-on module nine months later, the additional licensing costs reached €800,000 annually.

Hidden costs multiply during capacity crises. Carrier integration costs blindside most procurement teams because vendors present API availability as "included" functionality. Reality shows that custom EDI mappings, API rate limits, and carrier-specific data formatting requirements cost €5,000-€50,000 per connection.

Barrier #2: The Vendor Consolidation Trap

Companies undergoing integration often experience 12-18 months of reduced innovation while they harmonize platforms and teams. Post-acquisition integration timelines typically span 12-18 months, during which platform development stagnates and support quality deteriorates.

The numbers paint a stark picture of market concentration. Descartes Systems Group today said it has acquired the transportation management solutions (TMS) software vendor 3GTMS for $115 million. The deal marks Descartes' 32nd acquisition since 2016. This aggressive consolidation pattern indicates further acquisitions ahead, not behind us.

Previously, WiseTech's focus has been mainly on logistics service providers. Now, with e2open's deep product offerings, domain expertise and customer base, we're expanding our product offering into global and domestic trade including demand, planning, channel, supply, transportation and logistics for buyers, importers, exporters, shippers, manufacturers and brand owners. This strategic shift creates uncertainty about European manufacturer priority during integration planning.

European-native alternatives offer consolidation resistance. Vendors like Cargoson, Alpega, and Transporeon maintain specialized European focus that mega-vendors often dilute post-acquisition. European-native vendors often provide better insulation against global consolidation dynamics while maintaining specialized corridor expertise.

Barrier #3: The Integration Complexity Nightmare

Legacy ERP integration challenges hit mid-market companies disproportionately hard because they lack the internal expertise to manage complex system integrations. ICS2 becomes mandatory from 1 January 2026, while basic API integrations cost €5,000-€15,000, while complex ERP connections exceed €50,000. But here's the uncomfortable truth your IT director isn't telling you: budget overruns hit 75% of European TMS implementations, and 66% of technology projects end in partial or total failure.

The technical requirements are expanding beyond traditional transport management. Carriers and importers must integrate ERP and TMS systems with the ICS2 platform, with failure to report potentially resulting in a fine of up to 5,000 euros, especially with a large volume of shipments.

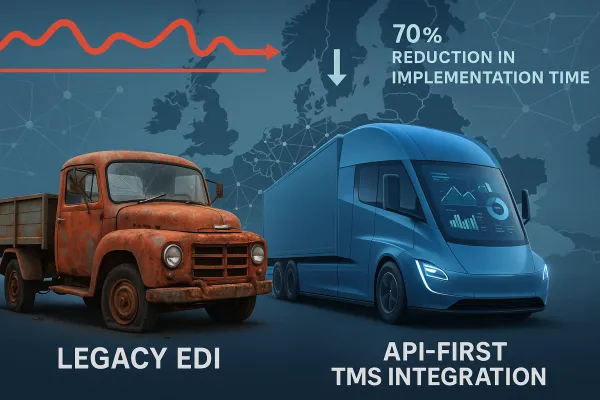

API-first platforms reduce integration complexity, but vendor selection matters enormously. Platforms like Cargoson, Manhattan Active, MercuryGate, and Descartes each bring different approaches to ICS2 compliance, but European-native solutions often provide better understanding of cross-border complexity and multi-country regulatory variations.

Barrier #4: The Skills Gap Reality

Mid-market companies face a double skills challenge: they lack both the logistics expertise to evaluate TMS capabilities properly and the technical expertise to implement them successfully. The services segment is projected to expand at a fastest CAGR of 11.4% from 2026 to 2034 owing to the increasing complexity of TMS deployments, the need for continuous system customization, and the rising demand for managed services among European shippers who can no longer afford the 66% of technology projects ending in partial or total failure.

The European IT skills shortage compounds this problem. The European Union General Data Protection Regulation threatens fines of up to 4% of global turnover for violations, prompting demands for data residency and control over encryption keys. Cloud providers have earned ISO 27001 and SOC 2 certifications, but internal security teams still run penetration tests and require detailed incident-response playbooks.

Services-led implementation approaches are becoming essential. Vendors offering comprehensive implementation support, training programs, and managed services help bridge the expertise gap that destroys mid-market implementations.

Barrier #5: The Procurement Timing Squeeze

The procurement window for securing optimal TMS platforms before vendor consolidation eliminates choices and capacity shortages worsen cost structures runs through Q1 2026. First, Europe's driver shortage is projected to triple by 2026 if no action is taken, creating capacity constraints that shift pricing power toward carriers and their technology partners. Second, companies that haven't initiated TMS selection processes by mid-2026 will find significantly fewer viable options as consolidation eliminates redundant platforms.

The regulatory timeline creates additional urgency. As of January 2026: eFTI platforms and service providers can start preparing for operations. As of 9 July 2027: The eFTI Regulation will apply in full. Member State authorities must accept information shared electronically by operators via certified eFTI platforms.

Procurement teams face a brutal choice: rush decisions to meet the window, or delay and face dramatically reduced options. Companies that haven't initiated TMS selection processes by mid-2026 will find significantly fewer viable options as vendors focus resources on existing customer compliance rather than new client acquisition.

The Strategic Response Framework for Mid-Market Success

European mid-market companies need acquisition-resistant procurement strategies that account for regulatory pressure, vendor consolidation, and implementation complexity simultaneously. The successful approach requires three parallel workstreams.

Financial protection starts with regulatory compliance guarantees. Vendors claiming eFTI readiness should demonstrate functional integration by January 2026, not just promise compliance by the July 2027 mandate. If a vendor can't deliver eFTI compliance by January 2026 or tachograph integration by July 2026, that's grounds for contract adjustment or termination.

Vendor stability assessment must extend beyond traditional financial metrics. Acquisition-resistant contracts require specific protections including 12-18 months advance notice for ownership changes, guaranteed functionality preservation for minimum periods, and migration assistance rights. Standard TMS contracts rarely address these scenarios, leaving mid-market buyers vulnerable to post-acquisition service degradation.

Implementation timing requires careful phasing. Cloud TMS implementations often conclude within eight weeks, compared to 6-18 months for traditional systems. Full value realization (integrations, training, adoption, process change) takes 4-6 months minimum. Start core functionality deployment in Q2 2026 to ensure readiness before regulatory deadlines create additional pressure.

Platform evaluation should consider the full vendor landscape while options remain available. This includes established platforms like MercuryGate, Descartes, E2open, Manhattan Active, Oracle TM, and SAP TM alongside European specialists like Alpega, nShift, Transporeon, and modern alternatives including Cargoson that focus specifically on European cross-border operations.

European shippers who act decisively within the next 90 days—with proper frameworks accounting for both capacity and consolidation scenarios—position themselves to navigate 2026's perfect storm successfully, while those who delay risk joining the statistics of failed implementations and budget overruns plaguing reactive procurement strategies.