The European Shipper's TMS Vendor Neutrality Assessment Framework: How to Build Bias-Proof Procurement Processes That Survive Consolidation When 66% of Selection Methods Fail Due to Hidden Vendor Dependencies

European transport directors managing €10+ million annual freight budgets face an uncomfortable truth. WiseTech Global's $2.1 billion acquisition of E2open and Descartes Systems Group's $115 million acquisition of 3GTMS represent the largest TMS vendor consolidation wave in market history, but most procurement teams still evaluate vendors like it's 2019. Meanwhile, 66% of technology projects end in partial or total failure, with 17% of large IT projects threatening company existence.

A German automotive manufacturer learned this the expensive way. After selecting their TMS based on a feature comparison spreadsheet, they faced €800,000 in additional costs when carrier integration failures emerged post-acquisition of their chosen vendor. Their mistake wasn't technical incompetence—it was using procurement frameworks that don't address the hidden bias and vendor dependency risks now plaguing European TMS selection.

The Hidden Bias Crisis in European TMS Procurement

Organizations remain vulnerable to polished sales presentations and hidden compliance gaps precisely when vendor neutrality matters most. Standard vendor scoring frameworks built around feature checklists, pricing comparisons, and current functionality miss the consolidation risks that now define procurement success. This creates dangerous exposure to vendor lock-in scenarios that European shippers can't afford during 2026's regulatory convergence.

The bias problem extends beyond procurement into operational reality. European shippers find themselves caught between global mega-vendors prioritizing enterprise accounts and specialized regional players with uncertain financial stability. Oracle TM and SAP TM provide comprehensive functionality but may deprioritize European-specific features during consolidation activities. Meanwhile, European specialists like Alpega, Transporeon, and modern alternatives including Cargoson offer rapid deployment and local expertise but face different acquisition pressures.

The Consolidation Accelerator Effect

Companies undergoing integration typically experience 12-18 months of reduced innovation while they harmonize platforms and teams. When vendor acquisitions happen mid-implementation, your project timeline extends while support resources get redistributed. This creates a procurement window running through Q1 2026—after which your leverage disappears as regulatory pressure forces decisions.

The timing creates additional complexity. Companies that haven't initiated TMS selection processes by mid-2026 will find significantly fewer viable options as vendors focus resources on existing customer compliance rather than new client acquisition. Your procurement decisions must account for this narrowing window while building frameworks that eliminate bias.

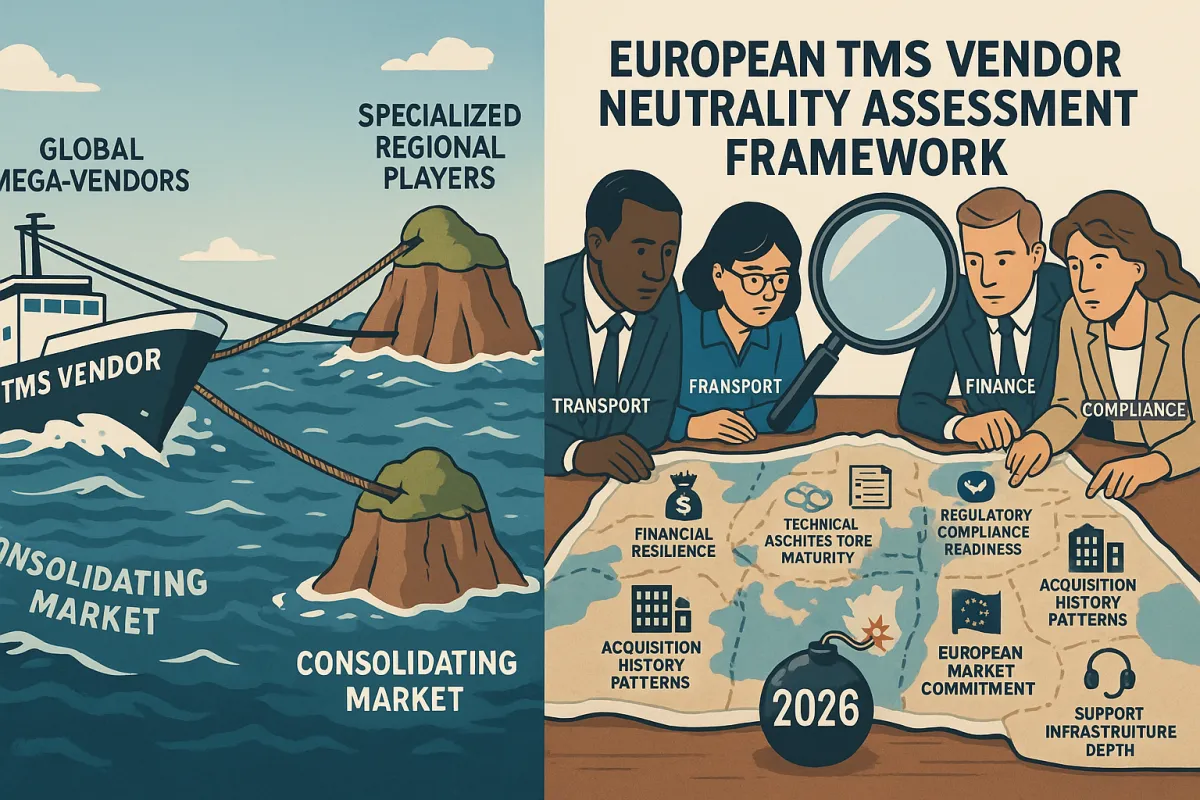

Building Your Vendor Independence Verification System

Independent consultants with vendor-agnostic approaches ensure objectivity and risk mitigation, but you need systematic frameworks that go beyond traditional evaluation methods. Replace feature-based scoring with a six-dimension framework that evaluates vendor stability beyond quarterly earnings reports: financial resilience, technical architecture maturity, regulatory compliance readiness, acquisition history patterns, European market commitment, and support infrastructure depth.

Multiple evaluators scoring independently reduce bias while documented rationale behind scores creates accountability. Your assessment matrix should weight these factors based on specific risk tolerance. A €50 million annual transport spend company cannot afford the same integration disruption risk as a €500 million operation. Build evaluation teams with representatives from transport, IT, finance, and compliance to prevent single-department bias from dominating vendor selection.

Financial Stability vs. Sales Presentation Assessment

Financial health indicators become critical evaluation criteria in a consolidating market. While WiseTech has demonstrated consistent profitability and growth, e2open has struggled with financial performance in recent years, reporting declining revenue and net losses in recent fiscal years. Look beyond vendor marketing materials to examine cash flow statements, debt-to-equity ratios, and acquisition history patterns.

Red flags include vendors actively seeking growth capital or rapid customer acquisition without proportional support infrastructure expansion. Examine cash flow statements, debt-to-equity ratios, and acquisition history to understand whether a vendor presents an attractive acquisition target. Companies with strong market positions but limited financial resources often become prime candidates for larger players seeking market share expansion.

The European Regulatory Compliance Independence Test

Vendors claiming regulatory readiness should demonstrate functional integration by January 2026, not just promise compliance by the July 2027 mandate. Authorities in all EU Member States will be required to accept electronic data when shared by businesses via eFTI-compliant platforms, creating hard deadlines for vendor capability verification.

European-specific requirements demand proof, not promises. eFTI Implementation: As of January 2026. Vendors claiming eFTI readiness should demonstrate functional integration by January 2026, not just promise compliance by the July 2027 mandate. This timeline separation allows you to evaluate actual implementation capabilities versus marketing commitments.

Proof-of-Performance vs. Marketing Promises

Regulatory readiness requires functional demonstrations of customs classification, IOSS integration, and eFTI preparation capabilities. From 1 July 2026, international freight transport performed by vans up to 3.5 tonnes enters the tachograph regime: second-generation smart tachographs (G2V2) become mandatory. Test vendors' ability to handle machine-readable format requirements and QR code generation for every shipment across all transport modes.

Live demonstration scenarios provide better assessment than reference calls. Integration complexity assessment should include actual data formatting tests, error handling validation, and system performance under typical load volumes. Vendors demonstrating native compliance features versus add-on modules show deeper commitment to European operations.

Contract-Level Independence Protection Mechanisms

Standard TMS procurement contracts rarely address vendor acquisition scenarios, leaving European shippers vulnerable to post-acquisition service degradation that can derail operations. Standard TMS procurement contracts don't address vendor acquisition scenarios, leaving European shippers vulnerable to post-acquisition changes without recourse. Acquisition-resistant contracts require specific protections including 12-18 months advance notice for ownership changes, guaranteed functionality preservation for minimum periods, and migration assistance rights.

Price protection clauses locking pricing for 24 months following ownership changes prevent vendors from using acquisitions to renegotiate terms. When their vendor introduced eFTI compliance as a premium add-on module nine months later, the additional licensing costs reached €800,000 annually for one German automotive parts manufacturer who learned this lesson the expensive way. Include separate budget line items for regulatory compliance costs, which vendors may attempt to charge separately after acquisition.

Multi-Vendor Strategy Development

Distribute functionality across multiple systems—core TMS from primary vendor supplemented by specialized solutions for specific European requirements. Consider hybrid approaches where core functionality relies on stable platforms while specialized European compliance features utilize regional vendors with stronger regulatory focus. This approach reduces single-vendor dependency while maintaining operational flexibility.

Data portability requirements and export procedures guarantee migration ability when vendor changes affect service quality. Balance between Oracle TM/SAP TM enterprise scope, Descartes/Blue Yonder capabilities, and focused solutions like Cargoson that emphasize European market focus. Multi-vendor preparedness reduces dependency risk through API-first architecture and standardized integration frameworks.

Implementation Timeline and Vendor Assessment Schedule

Your procurement timeline should align with regulatory deadlines while avoiding the rush that leads to poor vendor selection. Start with core functionality in Q2-Q3 2025, activate AI features in Q4 2025, and ensure eFTI compliance by Q1 2026. Phase your evaluation to balance risk with operational requirements while maintaining vendor independence throughout the process.

Days 61-90 should emphasize technical evaluation focusing on integration flexibility and vendor independence. Financial stability assessment comes first, followed by carrier integration testing and TCO modeling that includes hidden compliance costs. A basic domestic shipper requires 10-15 integrations minimum, potentially totaling 1,000-1,500 hours of labor. For shippers with freight spend exceeding $250M annually, implementation can cost 2-3 times the subscription fee.

Ongoing Independence Monitoring Framework

Proactive relationship management maintains negotiation leverage throughout contract lifecycle while preventing vendor drift. KPI tracking and performance measurement integration should connect directly to contract terms. Automatic escalation procedures activate when performance drops below contractual thresholds, triggering vendor remediation requirements or contract adjustment rights.

Schedule quarterly business reviews that assess vendor performance against contract commitments and market alternatives. Maintaining negotiation leverage throughout the contract lifecycle requires proactive relationship management, not reactive problem-solving. Schedule quarterly business reviews that assess vendor performance against contract commitments and market alternatives. Regular audit cycles become mandatory as European transport regulations continue evolving rapidly, requiring vendors to maintain compliance capabilities without degrading independence.

The vendor neutrality assessment framework you build today determines whether you navigate 2026's consolidation wave successfully or join the growing list of budget disasters. European shippers who act decisively secure favorable contract terms and compliance-ready platforms before market consolidation eliminates choice. Those who delay face increasingly limited options as regulatory deadlines approach and vendor acquisition activity accelerates.