The 2026 Gartner Magic Quadrant TMS Shakeup: How European Shippers Can Navigate Vendor Consolidation and Regulatory Pressure to Secure Acquisition-Resistant Platforms Before Market Power Shifts Permanently

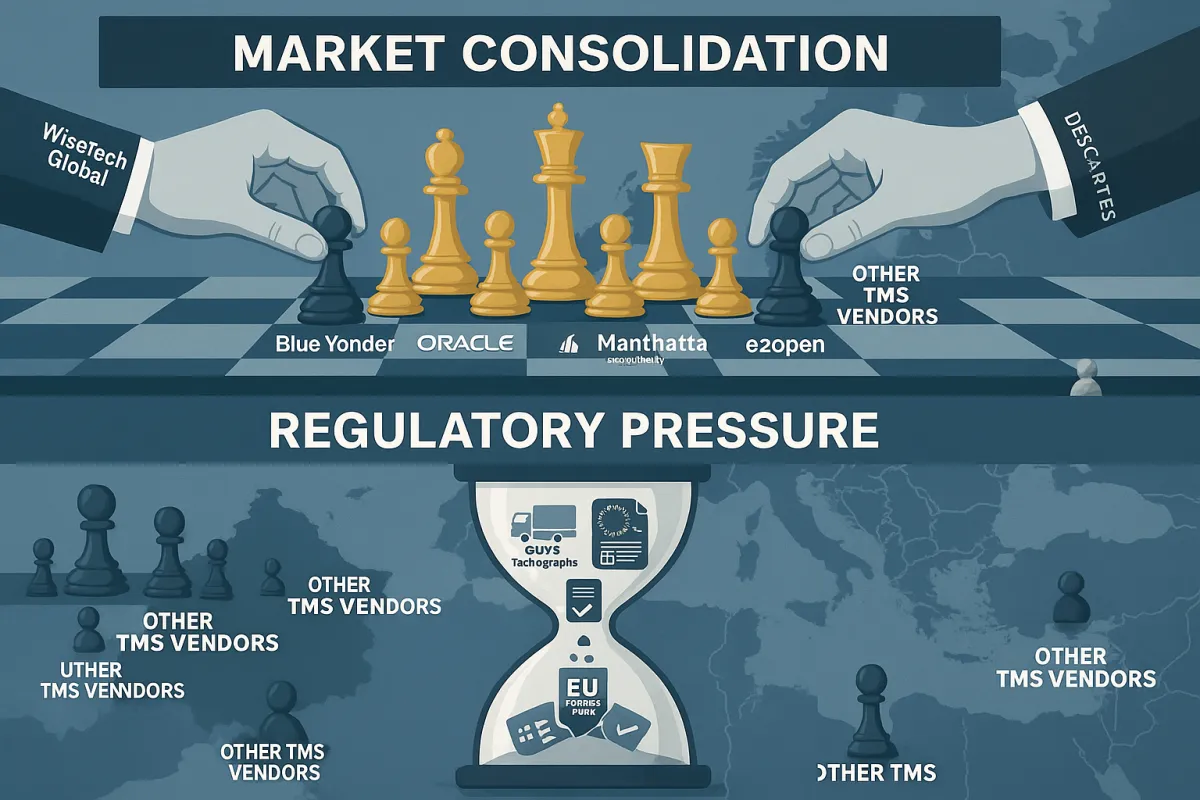

The 2026 Gartner Magic Quadrant for Transportation Management Systems, published March 30, 2026, lands in the middle of the most aggressive vendor consolidation wave the industry has ever seen. WiseTech Global's completed $2.1 billion acquisition of E2open and Descartes' $115 million purchase of 3GTMS, marking the Canadian company's 32nd acquisition since 2016, signal a fundamental shift in how European shippers need to approach TMS procurement.

For European transport directors managing €10+ million annual freight budgets, this isn't just another technology report to file away. With eFTI platforms preparing for operations starting January 2026 and G2V2 tachographs becoming mandatory for 2.5-3.5 tonne vans performing international goods transport from July 2026, you're being forced to make critical TMS decisions precisely when your vendor options are disappearing fastest.

The 2026 Magic Quadrant Reveals an Industry in Unprecedented Transition

Sixteen vendors were evaluated on their Ability to Execute and Completeness of Vision, with Blue Yonder named a Leader for the 19th consecutive time. Oracle was recognized as a Leader for the 19th time, while SAP earned Leader status for the 12th consecutive year. Manhattan Associates was named a Leader for the eighth consecutive year, and e2open was positioned as a Leader (now part of WiseTech).

What makes 2026 different is the market's evolution toward what Gartner describes as increasingly sophisticated functionality. Vendors are leveraging artificial intelligence, particularly GenAI and agentic AI, to differentiate their products, while the challenges of orchestrating end-to-end processes have increased the importance of transportation and supply chain execution convergence.

But here's what procurement teams miss: Gartner highlights AI agents automating routine tasks such as appointment scheduling, exception handling, and freight procurement, alongside the convergence of transportation with broader supply chain execution. This isn't future-state thinking—it's the baseline expectation for platforms that will survive the next 24 months of market consolidation.

The €2.1 Billion Consolidation Wave Reshaping European Procurement

WiseTech's $2.1 billion acquisition of e2open adds extensive cloud-based networks and customer reach with very little product overlap globally. More importantly for European buyers, this expands WiseTech beyond its traditional logistics service provider focus into global and domestic trade including transportation for buyers, importers, exporters, shippers, manufacturers and brand owners.

Descartes' 32nd acquisition since 2016 demonstrates a different consolidation model—systematic capability building rather than transformational market expansion. When you examine companies undergoing integration experiencing 12-18 months of reduced innovation while harmonizing platforms and teams, the distinction matters for your procurement timeline.

The consolidation impact hits European operations specifically. Consider that e2open's acquisition includes legacy platforms like INTTRA responsible for around 25% of global ocean bookings. When two TMS platforms merge, you face decisions about system standardization, feature deprecation, and support duration—often without controlling the timeline.

Three Post-Consolidation Vendor Categories

The market now divides into distinct categories with different risk profiles. Global mega-vendors (Oracle TM, SAP TM, E2open/WiseTech, Descartes), European specialists (Alpega, nShift, Transporeon), and emerging European-native solutions like Cargoson that maintain development focus specifically on European regulatory requirements.

Global mega-vendors provide comprehensive functionality and financial stability, but traditional providers like SAP TM and Oracle often struggle with localized European requirements. European specialists maintain development resources focused exclusively on European market needs, while global vendors spread development efforts across multiple geographic priorities, translating into faster feature development for European-specific requirements.

Modern European platforms like Cargoson alongside established options including Alpega and Transporeon offer rapid deployment advantages, but require evaluation of acquisition resistance and long-term scaling capabilities.

2026 Regulatory Deadlines That Compound Procurement Complexity

European transport faces multiple simultaneous regulatory changes that TMS platforms must support. From July 1, 2026, vans weighing 2.5-3.5 tons performing international transport will require G2V2 tachographs, while January 1, 2026 marked the end of CBAM's transitional phase with importers now subject to full financial obligations.

The AES/ECS2 PLUS system became operational across the EU in 2026, replacing existing export procedures with electronic-only export declarations. Additional deadlines include ADR enforcement by June 2026, digital ECMT permits from January 2026, and progressive eFTI platform certification starting January 2026.

The financial impact extends beyond device costs. Installation costs for G2V2 tachographs can reach €3,500-€4,700 per vehicle when combined with software purchases and employee training. Companies must account for purchasing and installing devices, driver and company card expenses, plus training costs.

2026 represents a stack of changes rather than isolated compliance requirements: dangerous goods enforcement, van tachograph requirements, new safety technology in heavy vehicles, and rising cost drivers including wages, tolls, and access restrictions.

Building Acquisition-Resistant Procurement Strategies

Standard TMS procurement contracts don't address vendor acquisition scenarios, leaving European shippers vulnerable to post-acquisition changes without recourse, requiring acquisition-resistant contracts with 12-18 months advance notice for ownership changes, guaranteed functionality preservation, and migration assistance rights.

Contract protection requires specific clauses beyond traditional terms. Include pricing protection through acquisition transitions with 24-month locks, feature deprecation rights preventing core functionality elimination, and data portability requirements ensuring migration flexibility. Build regulatory deadlines directly into implementation timelines with penalty clauses—if vendors can't deliver eFTI compliance by January 2026 or tachograph integration by July 2026, that's grounds for contract adjustment.

Financial stability assessment becomes as important as feature evaluation. While WiseTech has demonstrated consistent profitability and growth, e2open struggled with financial performance in recent years. Look beyond vendor marketing to examine cash flow statements, debt-to-equity ratios, and acquisition history patterns, with red flags including vendors seeking growth capital without proportional support infrastructure expansion.

Strategic Vendor Evaluation Beyond Traditional Criteria

Standard vendor scoring frameworks built around feature checklists and pricing comparisons miss consolidation risks that now define procurement success, creating dangerous exposure to vendor lock-in scenarios during 2026's regulatory convergence.

European market commitment indicators matter more than global feature breadth. European TMS vendors like Alpega and Cargoson offer regional focus advantages including dedicated European development teams, local regulatory expertise, and market-specific feature development priorities, typically providing faster eFTI implementation and better cross-border carrier connectivity.

Regulatory compliance roadmap evaluation should separate marketing promises from actual capabilities. Vendors claiming regulatory readiness should demonstrate functional integration by January 2026, not just promise compliance by the July 2027 mandate. This timeline separation allows you to evaluate actual capabilities rather than development commitments.

Platforms demonstrating native eFTI integration, automated tachograph data processing, and integrated CBAM compliance show commitment to European operations, while vendors treating European compliance as secondary requirements reveal prioritization during resource allocation decisions.

The Q1 2026 Procurement Window: Why Timing Matters

Timeline pressure intensifies beyond 2026, with companies that haven't initiated TMS selection processes by mid-2026 finding significantly fewer viable options as consolidation eliminates redundant platforms. The procurement window for securing optimal TMS platforms before vendor consolidation eliminates choices runs through Q1 2026.

Budget planning must account for regulatory complexity: plan for 15-20% budget increases in 2026-2027 if reactive, or 8-12% if proactive with proper contract protection, reflecting mandatory eFTI integration, G2V2 tachograph connectivity, and enhanced customs documentation requirements.

The leverage mathematics favor early movers. Vendor sales cycle timing creates pressure points that improve negotiation outcomes, with quarter-end and year-end deadlines providing natural leverage opportunities while regulatory deadline pressure creates additional urgency benefiting prepared buyers.

European shippers who act decisively within the next 90 days—with proper frameworks accounting for both capacity and consolidation scenarios—position themselves to navigate 2026's perfect storm successfully, while those who delay risk joining the statistics of failed implementations and budget overruns plaguing reactive procurement strategies.

The 2026 Gartner Magic Quadrant for TMS provides the framework for evaluation, but European success depends on understanding how vendor consolidation and regulatory convergence transform traditional procurement approaches. Your next TMS decision will likely be your last for the next 5-7 years. Choose accordingly.