The €400,000 Native Telematics Revolution: How European Shippers Can Eliminate Hardware Costs and Cut TMS Implementation Time by 60% While Building Future-Proof Transport Management Before Traditional Integration Models Collapse

The European transport industry is experiencing a perfect storm of regulatory requirements that make native telematics integration with TMS platforms not just a competitive advantage, but an operational necessity by 2026. Geotab's March 2026 partnership with Hyundai across 40+ European markets demonstrates how OEM-embedded telematics eliminates aftermarket equipment and installation expenses entirely, marking the beginning of a fundamental shift away from costly hardware retrofits.

Your TMS procurement decision this year determines whether you're ahead of the €400,000 implementation cost curve or caught in it. Budget overruns hit 75% of European TMS implementations, with complex ERP connections exceeding €50,000 while basic API integrations cost €5,000-€15,000. Yet the number of active telematics devices in Europe is expected to reach 49.77 million by 2026, creating a massive data explosion most European shippers haven't properly budgeted for.

The Native Telematics Integration Breakthrough Transforming European TMS Procurement

Native integration leverages OEM-embedded telematics already built into supported vehicle models, transmitting data seamlessly to platforms without retrofitting additional hardware, offering significant cost advantages by eliminating aftermarket equipment and installation expenses. This isn't just about cost savings—it's about data quality and implementation speed.

The partnership provides customers with instant access to high-quality vehicle data, from precision safety metrics to critical battery insights, with 10-second GPS updates and predictive maintenance capabilities. Compare this to traditional aftermarket installations that require weeks of downtime, hardware procurement, and integration complexity.

Major TMS vendors are taking different approaches to this integration challenge. Trimble's cloud-native platform integrates telematics data directly into dispatching and planning modules, utilizing automated workflows to handle routine tasks while providing a technical foundation for fleet management. Manhattan Active's 2026 roadmap prioritizes "autonomous orchestration," where systems automatically re-route shipments and adjust warehouse schedules to match new arrival times. European specialists like Alpega, Transporeon, nShift, and Cargoson are building regulatory-first approaches designed specifically for cross-border European complexity.

Why Traditional Aftermarket Telematics Integration is Becoming Obsolete

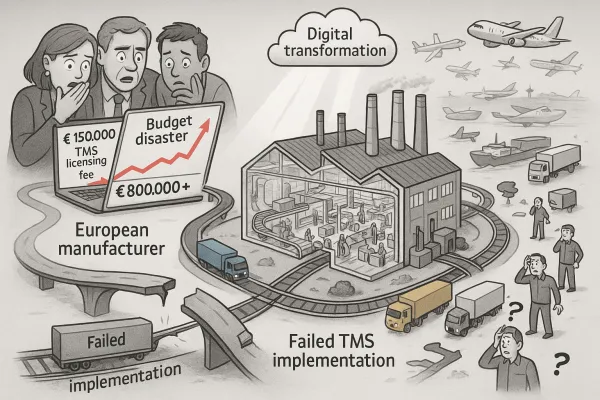

The numbers reveal the true cost of traditional integration approaches. Enterprises running SAP ECC or Oracle E-Business Suite incur integration bills of USD 500,000 to USD 3 million when layering a cloud TMS, with Manhattan Associates reporting an 18% year-over-year increase in professional services revenue from integration projects. A German automotive parts manufacturer discovered their €800,000 TMS implementation couldn't handle their complex carrier network across 12 European countries six months into deployment.

These failures aren't outliers—they're predictable outcomes when companies evaluate integration requirements using simple software selection criteria. High implementation costs remain a primary barrier, especially for SMEs, as enterprise-grade TMS platforms require configuration, data migration, staff training, and integration with existing systems, with many organizations delaying upgrades due to budget constraints or limited internal IT capabilities.

Meanwhile, native telematics integration is already available across more than 40 European markets, including the UK, Germany, France, Spain, Italy, the Netherlands, Poland, Norway, Sweden, and Ireland, providing immediate access without the traditional implementation nightmare.

The Regulatory Convergence Making Native Integration Mandatory

The regulatory drivers make this transformation unavoidable, with the forthcoming Euro 6e-bis emissions standard and smart tachograph Gen2V2 fitment by July 2026 ensuring all commercial vehicles will carry advanced telematics. From July 1, 2026, smart tachograph version 2 becomes mandatory for commercial vehicles over 2.5 tons in cross-border traffic, extending EU tachograph rules to the van segment for the first time.

The Gen2V2 includes a mandatory ITS interface with Bluetooth connectivity for secure data exchange with third-party systems, meaning fleet telematics platforms can pair with the tachograph to access vehicle location, speed, driver activity, and vehicle events in real time. This creates an unprecedented opportunity for native data integration directly from regulatory-required equipment.

The eFTI Regulation applies in full from 9 July 2027, requiring Member State authorities to accept information shared electronically by operators via certified eFTI platforms. Member States authorities may start accepting data stored on certified eFTI platforms for inspection from January 2026, with QR code generation and machine-readable format requirements becoming mandatory by July 2027, requiring TMS platforms to generate these automatically for every shipment across all transport modes.

European specialists like nShift, Transporeon, Alpega, and Cargoson often provide more transparent pricing models built specifically for cross-border European operations, while major vendors like Oracle TM and SAP TM price complex ERP connections based on data volume and customization requirements.

The €1 Billion eFTI Opportunity Hidden in Vehicle Data

The European Commission estimates the eFTI shift could save the EU logistics sector up to €1 billion per year. With estimated cost savings of up to €1 billion per year for the EU transport and logistics sector through lower compliance costs for businesses via automated data exchange and contribution to sustainability goals by eliminating paper waste.

Native telematics integration becomes the foundation for automatic compliance documentation. Connection with telematic systems provides fleet managers with constant access to driver status and tachograph data in near real-time, allowing ongoing monitoring of location, working time, and rest periods, with systems automatically sending notifications when drivers approach working hour limits.

Digital freight documentation could eliminate around 160 million paper sheets per year, with eCMR supporting better route planning and real-time visibility, helping carriers and shippers improve fleet utilization and reduce empty runs. This isn't just compliance—it's operational transformation.

Native Telematics Integration Vendor Evaluation Framework

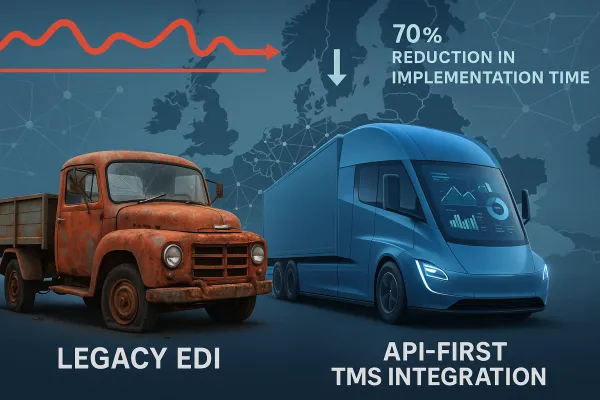

Evaluating true native integration capabilities requires looking beyond marketing claims. Start with data frequency and API maturity. True native integration provides 10-second GPS updates, precision safety metrics, and critical battery insights, not the 5-minute intervals typical of aftermarket solutions.

Examine hardware elimination thoroughly. Genuine native integration leverages OEM-embedded telematics already built into supported models, eliminating aftermarket equipment and installation expenses. If a vendor mentions "minimal hardware" or "simple installation," they're not offering true native integration.

Assessment criteria should include: real-time data access frequency, OEM partnership depth, regulatory compliance automation, multi-modal support for eFTI requirements, and API quality for third-party integrations. Vendors differentiate on the depth of carrier integrations, with Project44 connecting 180 telematics providers by 2025, while Descartes built SmartWay emission calculators directly into freight-audit workflows.

Compare Oracle's enterprise focus with SAP's ERP integration strengths, Blue Yonder's AI planning capabilities, and Trimble's fleet-centric approach. European alternatives like Cargoson, Alpega, Transporeon, and nShift often provide better understanding of cross-border complexity and regulatory variations specific to European operations.

The Multi-Vendor Fleet Management Challenge

Most European fleets operate mixed vehicle portfolios from different OEMs, each with proprietary telematics systems. The Geotab integration is available across more than 40 European markets, but covers only Hyundai vehicles. Your TMS needs to handle data from Volvo, Mercedes, Scania, and other manufacturers simultaneously.

Brand-agnostic platforms offer unified fleet management but often sacrifice data depth. Single-OEM solutions provide richer data but create operational silos. The optimal approach combines a core TMS capable of normalized data processing with OEM-specific integrations where available.

The collaboration allows fleets to manage their entire portfolio of vehicles—including internal combustion engines and electric vehicles—within a single, unified environment, with harmonized native vehicle data and advanced analytics providing consolidated operational views. This unified approach becomes more valuable as fleets electrify and diversify.

Implementation Strategy and Cost-Benefit Analysis

Start with a phased migration approach that validates core functionality before adding complex integrations. European operations often see 15-25% improvements in transport administrative efficiency within the first year of successful TMS data integration, with improvements coming from reduced manual data entry, automated compliance reporting, and enhanced visibility across transport networks.

Cloud-based solutions offer distinct advantages, often proving more cost-effective than on-premise deployment mainly because licensing and data storage system costs are lower, with less required technical labor. This becomes particularly relevant for native telematics integration, where data volumes can scale dramatically.

ROI calculation frameworks must extend beyond simple cost reductions. Track operational improvements like reduced manual data entry, faster carrier onboarding, improved compliance reporting accuracy, and enhanced visibility across your transport network. Factor in real-time alerts that allow fixing issues before they become Fixed Penalty Notices and DVSA Earned Recognition opportunities that reduce roadside stops through high-level reporting and data integrity.

Consider timing strategically. Member States authorities may start accepting data stored on certified eFTI platforms for inspection from January 2026—use this voluntary period for real-world testing and staff training. Carriers who are already running eFTI-conformant platforms by mid-2026 will spend the second half of 2026 helping their customers transition, while carriers who wait will be told by customers which platform to use.

Avoiding the Vendor Lock-In Trap

WiseTech Global's $2.1 billion acquisition of E2open and Descartes Systems Group's $115 million acquisition of 3GTMS represents significant vendor consolidation, with companies undergoing integration often experiencing 12-18 months of reduced innovation while harmonizing platforms. When vendor acquisitions happen mid-implementation, project timelines extend while support resources get redistributed.

Contract negotiation strategies must include data portability requirements, API access guarantees, and termination clauses that protect against sudden platform changes. Plan for 15-20% budget increases in 2026-2027 if reactive, or 8-12% if proactive with proper contract protection.

Maintain flexibility by implementing standardized data formats and avoiding vendor-specific customizations where possible. European regulatory expertise varies significantly between platforms, with European-native solutions like Cargoson, Manhattan Active, MercuryGate, and Descartes each bringing different approaches to ICS2 compliance.

Future-Proofing Your Native Telematics Strategy for 2027 and Beyond

Artificial Intelligence and Machine Learning are changing TMS platforms, making smarter, data-driven decisions possible using logistics data, with TMS and ML platforms providing automated routing and scheduling based on predictive modeling, including traffic, weather, shipment history, and capacity patterns, while predictive analytics capabilities evolve to increase proactive capabilities.

Autonomous vehicle integration will depend heavily on native telematics capabilities. Today's OEM-embedded systems provide the foundation for tomorrow's autonomous fleet management. Platforms like Uber Freight's TMS merge institutional logistics power with high-speed AI capabilities, standing out because systems self-manage tendering, scheduling and carbon tracking, reducing manual overhead through 30 embedded AI agents, with modular architecture allowing rapid same-day integration.

Predictive maintenance capabilities represent immediate value from native integration. Second-generation smart tachographs include functions for recording loads and unloads in tachograph memory and on driver cards, with driver menus including options to mark these activities along with automatic recording of time and location, streamlining logistics management and eliminating manual documentation.

In 2026, transportation management becomes the strategic backbone that connects demand signals with real-time execution, customer experience, and cost control, with modern supply chains demanding smarter decision-making, deeper automation, better visibility, and next-generation transportation management technology. Companies implementing native telematics integration now position themselves for sustained competitive advantage as the industry transforms around regulatory requirements and technological capabilities.

The competitive landscape favors early adopters, with companies implementing eFTI-compatible systems now gaining operational advantages while competitors struggle with compliance deadlines, while solutions from providers like Cargoson, nShift, Descartes, and emerging technologies position forward-thinking shippers for sustained competitive advantage. The July 2027 deadline approaches faster than most procurement cycles allow, making 2026 the year for strategic TMS decisions that will define your transport operations for the next decade.