The European Shipper's Essential Guide to Acquisition-Resistant TMS Contracts: How to Secure Bulletproof Protection Clauses Before Vendor Consolidation Eliminates Your Negotiation Leverage

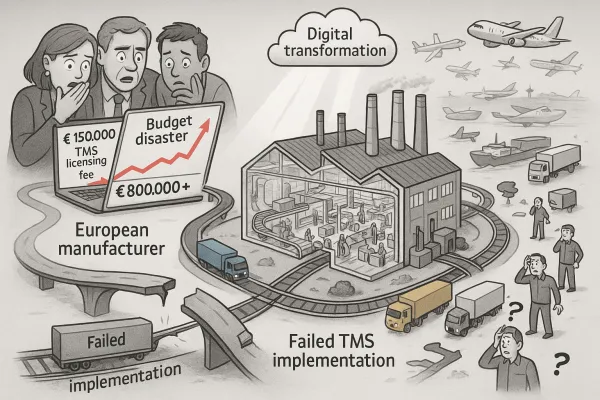

A German automotive manufacturer learned about vendor acquisition risks the expensive way. After selecting their TMS based on a feature comparison spreadsheet, they faced €800,000 in additional costs when WiseTech Global completed its strategic acquisition of e2open for an enterprise value of $2.1 billion triggered unexpected integration requirements. Their chosen vendor's platform merged with a competing system, forcing them to rebuild carrier integrations and migrate data they thought would remain stable for years.

Sound familiar? WiseTech's acquisition of E2open in 2025, Descartes' purchase of 3GTMS for $115 million in March 2025, and Körber's transformation of MercuryGate into Infios following their 2024 acquisition represent just the beginning of a fundamental market restructuring that's forcing European shippers to reconsider their entire approach to acquisition-resistant TMS contracts.

You face a dangerous combination: regulatory deadlines approaching, vendor consolidation accelerating, and 66% of technology projects end in partial or total failure, while 17% of large IT projects go so badly, they threaten the very existence of the company. When your TMS vendor becomes an acquisition target, you inherit these integration risks without directly managing the project.

The Vendor Consolidation Crisis Creating Contract Vulnerabilities

The supply chain technology industry witnessed its most significant transaction of the year when WiseTech Global announced its acquisition of e2open for US $2.1 billion, but this deal represents more than a simple market transaction. The companies offer competing solutions in what may be the largest overlap of all: TMS and global trade solutions for the forwarding and LSP markets, creating exactly the type of platform consolidation scenario that European procurement teams haven't adequately protected against.

The deal marks Descartes' 32nd acquisition since 2016, demonstrating how aggressive the consolidation trend has become. Meanwhile, Descartes Systems Group acquired 3GTMS for $115 million, marking their 32nd acquisition since 2016, while WiseTech's strategic acquisition of E2open combines two of the most acquisitive players in this space. The pattern is clear: mid-market European TMS providers with specialized capabilities face acquisition pressure from global mega-vendors seeking geographic expansion and feature consolidation.

Consider what happens during these acquisitions. Both platforms serve similar customer segments with overlapping functionality, leaving questions about which solutions (and customers) win. Traditional contracts don't address these ownership changes because most procurement teams focus on feature requirements rather than corporate stability during vendor selection.

European suppliers like Cargoson, Alpega, and nShift represent attractive acquisition targets precisely because they've built strong regional capabilities that global vendors lack. European specialists maintain development resources focused exclusively on European market needs, while global vendors like Descartes or WiseTech spread development efforts across multiple geographic priorities. This specialization makes them valuable acquisition targets but creates risks for customers who selected them for those specific European-focused capabilities.

Why Standard TMS Contracts Fail During Acquisitions

Your current TMS contract probably includes standard provisions for software updates, support response times, and feature availability. What it doesn't include are protections for what happens when your vendor gets acquired and platform consolidation begins.

For e2open customers, the main concern is whether WiseTech will maintain innovation and product investment during the integration. This represents the core vulnerability in standard contracts: they assume vendor continuity rather than preparing for ownership disruption.

When two TMS platforms merge, customers inevitably face decisions about which system to standardize on, what features will be deprecated, and how long dual support will continue. These transitions often require additional implementation costs, data migration expenses, and integration redevelopment that weren't included in original total cost of ownership calculations.

The financial impact gets severe quickly. About 19% of software projects result in complete failure, with 49% facing budget overruns, while 17% of IT projects risk collapsing the company itself. During vendor acquisitions, these failure rates increase because you're essentially forced into an unplanned system migration or integration project with compressed timelines and limited vendor resources.

Standard contracts also fail to address regulatory compliance during transitions. European operations face eFTI implementation deadlines and G2V2 tachograph requirements that don't pause for vendor consolidation activities. If your TMS vendor gets acquired and integration disrupts compliance capabilities, you bear the regulatory risk while having minimal control over the technical resolution timeline.

The Essential Acquisition Protection Clauses Every Contract Needs

Advance Notification Requirements

Acquisition-resistant contracts require specific protections including 12-18 months advance notice for ownership changes, guaranteed functionality preservation for minimum periods, and migration assistance rights. This notification period isn't arbitrary – it reflects the time needed to evaluate alternatives, negotiate termination if necessary, or prepare for platform transitions.

Your contract should specify that "material ownership change" includes any transaction where more than 25% of voting control transfers to a new entity, merger announcements, or acquisition due diligence processes that could affect your service level agreements. The acquisition is expected to be completed in 1H26, subject to applicable regulatory approvals, while E2open and WiseTech will continue to operate as independent companies until the transaction closes, demonstrating how acquisition timelines provide advance warning that contracts should leverage.

Pricing Protection During Transitions

Your contracts should include pricing protection clauses that lock rates for 24 months following any vendor ownership change. This protection prevents acquiring companies from immediately raising prices to fund acquisition costs or align with their existing pricing models.

Specify that pricing protection applies to base software licensing, support fees, professional services rates, and any third-party integration costs. Include automatic renewal terms that prevent forced contract renegotiation during transition periods when your negotiation leverage is weakest.

Feature Deprecation Rights

Feature deprecation rights protect against post-acquisition platform consolidation that eliminates capabilities European operations require. Include contractual guarantees for feature availability, performance benchmarks, and alternative solution provision if acquired vendors discontinue functionality critical to European regulatory compliance or operational requirements.

These clauses should specify minimum support periods (typically 18-24 months) for any features marked for deprecation, plus requirements for equivalent replacement functionality or assisted migration to alternative solutions. The parcel management space shows redundancy, with e2open's multi-carrier parcel solutions overlapping with WiseTech's parcel platform, illustrating how acquisition-driven feature consolidation creates exactly the risks these clauses address.

Using Regulatory Deadlines as Contract Leverage

eFTI, G2V2, and CBAM requirements create vendor pressure you can exploit during contract negotiations. Vendors claiming regulatory readiness should demonstrate functional integration by January 2026, not just promise compliance by the July 2027 mandate. This timeline separation allows you to evaluate actual capabilities rather than marketing promises.

Structure penalty clauses around compliance milestones that increase vendor accountability. For example, include specific financial penalties if eFTI integration fails testing by predetermined dates, or if G2V2 tachograph connectivity doesn't meet specified performance thresholds during pilot phases.

The regulatory pressure works in your favor because vendors face European market exclusion if they don't deliver compliance capabilities. European specialists maintain development resources focused exclusively on European market needs, making them more motivated to accept stringent compliance-based contract terms than global vendors managing multiple geographic priorities.

Include specific language requiring vendors to maintain regulatory compliance capabilities even during acquisition transitions. This prevents acquiring companies from deprioritizing European-specific features during platform consolidation phases.

Vendor Financial Health Assessment for Contract Security

Mid-market TMS providers with specialized European capabilities but limited global reach represent higher acquisition risk than either dominant market leaders or small niche players. The sweet spot for acquisitions typically includes companies with €10-50 million annual revenue and established customer bases in attractive geographic markets.

Evaluate vendors like Cargoson, Alpega, and nShift differently than Oracle TM or SAP TM when assessing acquisition risk. European specialists face pressure from global vendors seeking regional expansion, while established mega-vendors like Oracle or SAP typically acquire for specific capabilities rather than geographic reach.

Red flags include recent private equity investments, frequent leadership changes, rapid expansion into new geographic markets, or aggressive pricing that seems unsustainable. Integration complexity of merging two SaaS platforms, sales teams, and partner ecosystems demands flawless execution, making vendors with complex organizational structures higher-risk acquisition targets.

Review vendor financial statements for debt levels, revenue concentration, and cash flow patterns. Companies with high customer concentration in specific industries or geographies become attractive acquisition targets when consolidating vendors want to enter those markets quickly.

The 90-Day Contract Negotiation Timeline

Companies that haven't initiated TMS selection processes by mid-2026 will find significantly fewer viable options as consolidation eliminates redundant platforms. As E2open and WiseTech move toward closing, the era of loosely connected supply chain software may be ending, making timing critical for securing acquisition-resistant contract terms.

Phase your approach across 90 days: financial assessment, regulatory compliance verification, and contract protection negotiation. Days 1-30 focus on vendor stability analysis and acquisition risk evaluation. Review vendor financial statements, ownership structure, and market positioning. Identify potential acquirers by analyzing which larger players lack capabilities in your vendor's specialization areas.

Days 31-60 concentrate on regulatory compliance verification and performance benchmarking. Test actual eFTI integration capabilities, verify G2V2 connectivity, and evaluate CBAM reporting functionality rather than accepting vendor assurances.

Days 61-90 finalize contract terms with acquisition protection clauses, pricing guarantees, and feature preservation requirements. Contract terms negotiation focused on consolidation protection should include acquisition notification requirements, price protection clauses, functionality guarantees, and termination rights.

Implementation Strategy with Acquisition Protection

Structure contracts to minimize disruption during vendor transitions by requiring temporary dual-platform access or enhanced support during transition periods. If acquired platforms require 18+ months for full integration, you need contractual guarantees for continued service levels rather than hoping acquiring vendors maintain support voluntarily.

Migration assistance requirements and data portability clauses become critical when vendors merge platforms. Include specific provisions for data extraction in standard formats, API access for third-party migration tools, and professional services availability for transition projects.

Evaluate vendors like MercuryGate (now Infios), Descartes, and E2open/WiseTech against European specialists like Cargoson for acquisition resistance based on ownership structure rather than just functionality. Publicly traded vendors face different acquisition pressures than privately held companies, while vendors with recent private equity investments often face sale pressure within 3-5 year timeframes.

Your implementation strategy should include escape clauses that activate during ownership changes, allowing contract termination without penalties if service levels, feature availability, or pricing change beyond specified thresholds. These clauses provide insurance against acquisition scenarios that make continued vendor relationships impractical.

The consolidation wave creating these risks won't wait for your convenience. More than two-thirds of large-scale tech programs are not expected to be delivered on time or within budget or to meet their defined scope, and vendor acquisitions increase these failure rates by forcing unplanned integration projects with compressed timelines. Protect your organization by negotiating acquisition-resistant contracts before market consolidation eliminates your negotiation leverage entirely.