The Hidden Cost Crisis Crushing European TMS Budgets: How to Identify the €200,000 Expense Categories Vendors Don't Disclose Before They Destroy Your Implementation

A German automotive manufacturer thought their €800,000 TMS budget was conservative until reality hit six months later. They discovered their new system couldn't handle their complex carrier network across 12 European countries, turning their "smart procurement decision" into a complete platform re-implementation. You face the same hidden cost crisis that's destroying European TMS budgets while unprecedented vendor consolidation eliminates your procurement options.

Hidden costs in TMS procurement consistently add 25-30% more than initial estimates, turning what looked like smart investments into budget disasters. 76% of logistics transformations fail to achieve their performance objectives because procurement teams focus on feature comparisons and license fees while the real financial impact lives in implementation complexity, carrier integration charges, and ongoing maintenance expenses.

The European TMS Hidden Cost Crisis That's Destroying Budgets

Budget overruns hit 75% of European TMS implementations, and these statistics are worsening precisely as regulatory pressure forces mandatory digital transformation. Here's what makes this worse: WiseTech completed the acquisition of E2open for $2.1 billion in August 2025, meaning integration disruption is happening right now for existing customers of both platforms. Meanwhile, Descartes Systems Group acquired 3GTMS for $115 million, marking Descartes' 32nd acquisition since 2016.

Why do traditional procurement frameworks miss these costs? Because software license is typically only 20–25% of total cost of ownership, with European shippers consistently underestimating TMS implementation costs by treating licensing like a simple software purchase rather than understanding it as a complex transformation affecting every carrier relationship. The German manufacturer's mistake wasn't unique—it reflects systematic gaps in how procurement teams evaluate implementation risk.

Vendor consolidation amplifies these cost pressures by reducing pricing transparency and extending integration timelines. When your TMS vendor becomes an acquisition target, you inherit integration risks without directly managing the project, with post-acquisition integration timelines typically spanning 12-18 months during which platform development stagnates.

The Five Hidden Cost Categories That Blindside European Procurement Teams

Carrier Integration Costs - The €50,000 Connectivity Trap

Carrier integration costs blindside most procurement teams because vendors present API availability as "included" functionality, but reality shows that custom EDI mappings, API rate limits, and carrier-specific data formatting requirements cost €5,000-€50,000 per connection. Many carriers aren't willing or able to create API connections, and even when they are, they'll charge integration costs to you, with European shippers working with 20-30 regular carriers facing substantial connectivity expenses that vendors rarely discuss during initial demos.

The complexity multiplies across European operations. Your TMS must handle French carriers using different API standards than German logistics providers, while Italian operators require separate EDI protocols. A basic domestic shipper needs 10-15 integrations minimum, totaling 1,000-1,500 hours of labor, while most shippers today require an average of 40 integrations with some complex implementations recording over 140 integration objects.

Different vendors handle this differently. Modern European providers like Cargoson build true API/EDI connections versus basic account setup. Manhattan's total cost of ownership ranks as relatively high, while cloud-native solutions like Cargoson focus on reducing implementation complexity through pre-built integrations and European carrier connectivity. Cargoson and other modern European TMS providers often include implementation support in their pricing models, contrasting with traditional enterprise vendors who separate these services, which impacts your total support costs over the system's lifecycle.

Legacy System Integration - The Enterprise Nightmare

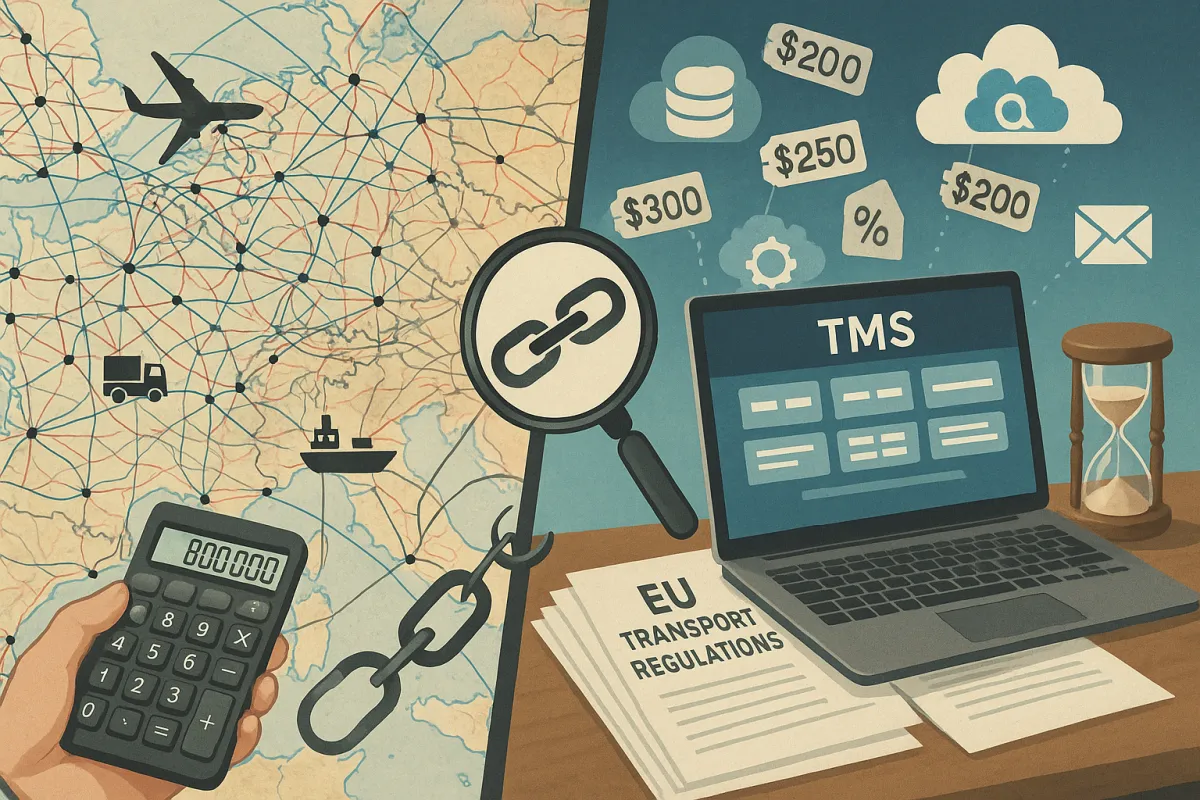

Enterprises running SAP ECC or Oracle E-Business Suite incur integration bills of USD 500,000 to USD 3 million when layering a cloud TMS, as legacy systems lack modern APIs, while your CFO sees the subscription fees—typically €1-4 per shipment for cloud solutions—but misses the integration reality.

Basic API integrations cost €5,000-€15,000, while complex ERP connections exceed €50,000. API-first platforms reduce integration complexity, but vendor selection matters enormously. The mid-market faces particular challenges because you lack internal expertise to manage complex system integrations while still requiring sophisticated functionality for multi-country operations.

Regulatory Compliance Costs - The European Penalty

European regulatory requirements add substantial expense layers that procurement teams consistently underestimate. Carriers and importers must integrate ERP and TMS systems with the ICS2 platform, with failure to report potentially resulting in a fine of up to 5,000 euros, especially with a large volume of shipments.

As of January 2026, eFTI platforms and service providers can start preparing for operations, while by December 2026, the Commission plans to adopt the remaining eFTI implementing specifications providing detailed functional and technical requirements for IT systems, with transport management systems claiming future compliance needing to demonstrate functional integration during 2026.

Starting August 19, 2025, all heavy-duty vehicles registered in the EU and operating in Member States other than their Member State of registration must be fitted with G2V2 devices. Regulatory compliance costs multiply your integration expenses through mandatory requirements like eFTI implementation, smart tachograph Gen2V2 connections, and EU ETS reporting capabilities, with your TCO calculator needing separate line items for eFTI compliance costs whether built into transaction fees or charged separately since the approaching mandate makes this a required expense.

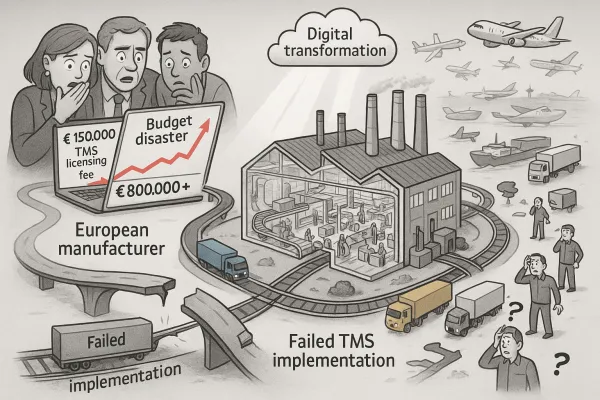

What catches teams off-guard: compliance should be baseline functionality, not premium add-ons. A German automotive manufacturer signed a three-year TMS renewal without regulatory compliance pricing protection, and when their vendor introduced eFTI compliance as a premium add-on module nine months later, the additional licensing costs reached €800,000 annually.

Implementation Services and Change Management

Implementation costs ranging from €30,000 to €900,000 require clear value definition and optimal outcome planning. For shippers with freight spend exceeding $250M annually, implementation can cost 2-3 times the subscription fee. The labor requirements are staggering when you account for European operational complexity.

Training costs depend on user adoption complexity and system interface design, with the expertise of the implementation team being critical since inadequate training leads to ongoing support tickets, user frustration, and reduced system utilization. Training and change management across multiple European countries creates another substantial cost layer, with properly trained employees being key to maximizing the benefits of your TMS and investing in comprehensive training preventing costly errors, as a manufacturing company that fails to adequately train its workforce on the new TMS might experience production line disruptions.

How Vendor Consolidation Amplifies Hidden Costs

WiseTech's acquisition of e2open for $2.1 billion marks the largest TMS industry acquisition to date, while Descartes' acquisition of 3GTMS for $115 million marks the 32nd acquisition since 2016. This creates a fundamentally different procurement environment where fewer vendors control more market share, reducing your negotiating leverage and pricing transparency.

Companies undergoing integration often experience 12-18 months of reduced innovation while they harmonize platforms and teams, with post-acquisition integration timelines typically spanning 12-18 months during which platform development stagnates and support quality deteriorates. During these periods, your feature requests get deprioritized while new customer acquisition slows.

The consolidation creates three distinct vendor categories for procurement planning: global mega-vendors (Oracle TM, SAP TM, E2open/WiseTech), European specialists (Alpega, nShift, Transporeon), and emerging European-native solutions like Cargoson that focus specifically on cross-border European operations. Each presents different cost structures and risk profiles.

While WiseTech has demonstrated consistent profitability and growth, e2open has struggled with financial performance in recent years, reporting declining revenue and net losses, meaning European buyers should evaluate vendor acquisition likelihood based on financial performance, market position, and strategic value to potential acquirers.

The European Shipper's Cost Control Framework

Pre-Procurement Cost Assessment

Build comprehensive TCO models that account for European operational complexity. The procurement strategy should evaluate total contract value over 5-7 years, not just year-one costs, and include scenarios for business growth, regulatory changes, and potential vendor acquisition that could affect pricing or service levels.

Consider these TCO components: base licensing (20-30% of total), implementation services (25-40%), carrier integration (15-25%), customization and training (10-20%), and ongoing support (15-20%). Your models must account for European-specific regulatory compliance costs as mandatory line items, not optional features.

Don't underestimate maintenance expenses. Licensed TMS models include annual maintenance charges ranging from 15-20% of license costs, while traditional software maintenance fees often run around 20% of the license fee annually for support and minor upgrades.

Contract Protection Strategies

Structure agreements that protect against consolidation risks. Standard TMS contracts rarely address acquisition scenarios directly, so include specific clauses requiring 12-18 months advance notice of ownership changes, with automatic contract review rights triggered by acquisition announcements.

Structure agreements with acquisition-resistant terms that include specific language requiring 12-18 months advance notice of any acquisition discussions, price protection during ownership transitions, and functionality guarantees that prevent feature deprecation without equivalent replacement.

Build regulatory compliance protection into your contracts. The eFTI compliance deadline creates procurement leverage that savvy buyers can exploit, with vendors needing your business to validate their eFTI implementations and demonstrate market traction to potential acquirers, so use this dynamic to secure better contract terms, comprehensive compliance support, and protection against post-acquisition changes.

Platform-Specific Cost Comparison for European Operations

Cloud versus licensed models present different economics for European operations. Cloud versus on-premise decisions significantly impact infrastructure costs, with modern cloud-based solutions from providers like nShift, Cargoson, and Transporeon eliminating hardware investments but introducing ongoing operational expenses, while on-premise implementations require hardware specifications, OS compatibility considerations, and dedicated IT team support.

European-native versus global platform costs vary significantly. European-focused platforms often provide better value through pre-built carrier connections and regional expertise compared to global solutions requiring extensive customization. Cargoson, Alpega, and other European specialists maintain development resources focused exclusively on European market needs while global vendors like Descartes or WiseTech spread development efforts across multiple geographic priorities, which translates into faster feature development for European-specific requirements.

When evaluating major platforms, consider both established vendors like Transporeon, Oracle TM, and SAP TM alongside emerging European-focused solutions such as Cargoson, nShift, and Alpega, with each category presenting different risk-reward profiles based on your specific operational requirements and integration complexity. Global mega-vendors provide comprehensive functionality and financial stability, but traditional providers like SAP TM and Oracle often struggle with localized European requirements, with their conversational AI modules built for global markets lacking nuanced understanding of European transport corridors.

The 2026 Procurement Window - Why Acting Now Controls Costs

This procurement window runs through Q1 2026, after which your leverage disappears as regulatory pressure forces decisions, with vendors shifting resources toward supporting existing customers through compliance requirements rather than competing for new implementations. The timing creates natural negotiation advantages for proactive buyers.

Budget planning around these timelines requires understanding both direct compliance costs and indirect operational impacts, with planning for 15-20% budget increases in 2026-2027 if reactive, or 8-12% if proactive with proper contract protection. Acting now gives you control over implementation timelines and vendor selection rather than accepting whatever capacity remains available.

Phase your implementation to balance risk with operational requirements by starting with core functionality in Q2-Q3 2025, activating AI features in Q4 2025, and ensuring eFTI compliance by Q1 2026, with TMS implementation usually taking 1-2 months for smaller shippers and 3-6 months for larger, more complex networks.

Companies that haven't initiated TMS selection processes by mid-2026 will find significantly fewer viable options as vendors focus on existing customer compliance rather than new acquisitions. Your options narrow as consolidation accelerates and regulatory deadlines approach.

Your 90-Day Action Plan to Avoid Budget Disasters

Days 1-30: Vendor Financial Stability Assessment

Start with financial stability assessment by looking beyond current revenue figures to understand how recent acquisitions impact the vendor's cash flow, development priorities, and customer service capacity. Look beyond vendor marketing materials to examine cash flow statements, debt-to-equity ratios, and acquisition history patterns, with red flags including vendors actively seeking growth capital or rapid customer acquisition without proportional support infrastructure expansion.

Days 31-60: Hidden Cost Audit and TCO Modeling

Establish 60-day checkpoints to validate integration progress and cost tracking while monitoring carrier onboarding speed, data quality metrics, and user adoption rates to identify budget risks before they become disasters. Build comprehensive spreadsheets tracking all potential costs over 5-7 year horizons.

Days 61-90: Contract Negotiation and Implementation Controls

Focus on acquisition-resistant contract terms and regulatory compliance protection. Smart buyers negotiate carrier integration costs upfront and prioritize TMS providers with extensive pre-connected networks to control connectivity expenses. Structure payment milestones tied to specific implementation achievements rather than time-based schedules.

Your success depends on understanding that European shippers can control TMS total cost of ownership through disciplined procurement practices that account for the full implementation lifecycle, not just subscription fees, with the difference between budget success and failure lying in understanding these hidden costs before the contract signature, not after the invoice arrives. The vendor consolidation wave gives you leverage now that won't exist in 2027.